A lot has changed in the past few years. Angry Birds became a national pastime. Tennessee fans are starting to fill football stadiums once again . China surpassed the United States to become the world’s largest economy. Innovative technologies disrupted whole industries. One thing hasn’t changed, though, and that is Americans’ generosity, especially when it comes to giving.

While it’s true that philanthropy suffered some setbacks following the financial crisis and Great Recession, Americans have given tens of billions of dollars to support charitable organizations. Between 2006 and 2012, more than $135 billion went to charity, according to a tax study by The Chronicle of Philanthropy, which accounted for about 80 percent of charitable gifts in the United States. Americans who earned more than $200,000 a year donated about $77.5 billion during the period, while Americans who earned less than $100,000 a year gave about $57.3 billion.

During 2013, Americans reached deeper into their pockets and gave even more. The 2014 U.S. Trust® Study of High Net Worth Philanthropy reported wealthy donors gave 28 percent more during the year. People earning between $1 and $5 million gave about $25,000, on average, while those earning more than $5 million gave about $166,600, on average. Americans also spent a lot of time – 200 hours or more for many study participants – volunteering.

I give, you give, they give

Although many studies of philanthropy focus on wealthier donors, it is clear philanthropy is not limited to wealthy Americans, large companies, or foundations. In fact, according to Philanthropy magazine, the vast majority of money given to charities each year comes from individuals – some are wealthy and some are not:

“The fireworks show that delighted your town this week. The children’s hospital where the burned girl from down the street was saved. The Rotary scholarship that allowed you to become dear friends with a visiting Indonesian graduate student. The church-organized handyman service that keeps your elderly mother in her home. The park that adds so much to your family life. These gifts, many of them products of small offerings from thousands of everyday residents, accumulate in powerful ways to make our daily existences safer, sweeter, and more interesting.”

Philanthropy is becoming a family affair, according to The New York Times, as parents strive to raise children who are socially responsible and understand the importance of giving and community service. “…Philanthropic giving is increasingly a family affair and children are getting involved at younger ages. Of the group with donor-advised funds – admittedly a group skewed toward the charitably inclined – 94 percent said they had taught or were teaching their children to give to charity.”

Rich and poor, young and old, Americans have been supporting diverse causes – education, basic needs, health, religious, arts, and others – which are near and dear to their hearts.

Altruistic and financial motivations

The reasons for making charitable gifts are probably as diverse as the people who make them. In fact, it’s likely many people give for more than one reason. Altruistic motivations – the sense of fulfillment gained by giving, the desire to make a difference in a community or the world, the drive to support political, religious, or philosophical beliefs – are often complemented by financial ones, including:

• Charitable tax deductions: Qualifying charitable donations, both cash and property, can be deducted when taxpayers itemize.

• Estate tax reductions: The National Council of Nonprofits pointed out the estate tax provides an incentive for wealthier Americans to “give back to their communities through nonprofit organizations.

• Charitable IRA rollovers: Through 2012, Americans age 70½ or older could have up to $100,000 sent directly from their Individual Retirement Accounts (IRAs) to charitable organizations. These distributions met required minimum distribution rules without creating taxable income for the IRA owner. The rule may be extended, but has not yet been.

• Land conservation easements: Through 2012, donors who give some or all of the development rights on a piece of land to a government agency or nonprofit, receive a federal income tax deduction. The rule may be extended, but has not yet been.

Some charitable tax benefits fall into the ‘tax extender’ category. These are pieces of legislation that expire and must be reapproved every few years. When this article was written it was unclear whether IRA rollovers and conservation easements would be extended into the current tax year.

Plans for giving

While not everyone has a plan for giving, many people have put strategies and budgets in place to guide their philanthropic efforts. The vehicles they employ to accomplish their goals vary significantly. Some have given online through crowdfunding platforms, but many opt for more traditional options, such as:

• A will: People become more philanthropic as they get older, according to Philanthropy. Giving often peaks between the ages of 61 and 75. One way older Americans give is by providing for a charity through his or her will.

• An endowment fund: One or more donors can leave money or property to a charitable institution with the expectation the assets will be invested and help finance the activities of the non-profit.

• A charitable remainder trust: Typically, assets are contributed to an irrevocable trust that pays income to donors and beneficiaries for a period of time (including a lifetime). Contributions to the trust generally are tax deductible.

• A charitable gift annuity: This is a contract and not a trust. In return for an irrevocable gift of assets, a charity agrees to pay an annuitant or beneficiary a stream of income over a lifetime. The donor receives a charitable tax deduction.

• A charitable lead trust: In general, assets are contributed to an irrevocable trust that pays income to a designated charity for a specific period of time. At the end of that time, any remaining assets go to the trust’s beneficiaries.

• A donor-advised fund: These are private funds that are administered by a third party and give the donor tax deductions as well as significant control over distributions to charities.

You may give a lot or a little. You may do it today or in the future. You may teach your children or find a sense of fulfillment. You may improve the world or gain a tax benefit. Regardless of the reasons, Americans have continued to give to the common good even when our economy has suffered – and that’s really something.

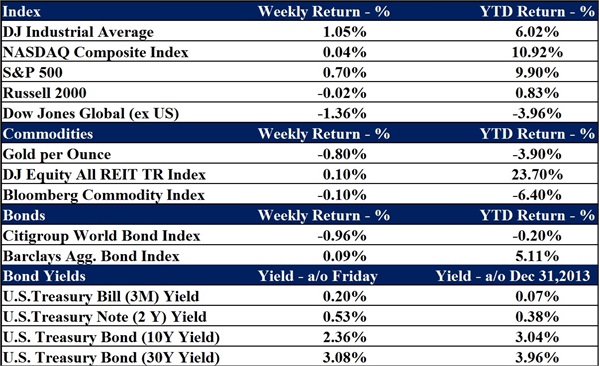

Data as of November 11th, 2014

Nick Hughes is a Wealth Advisor with Franklin Wealth Management, a registered investment advisory firm in Hixson, Tennessee. In addition to advising clients since 2007, he has contributed to articles for Market Watch and FinancialPlanning.com and is a regular contributor to the Franklin Backstage Pass blog.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.