It seems that every year in December we get a multitude of calls from clients regarding a pretty common occurrence for mutual funds, but nonetheless an often misunderstood one. December is the time of year when most mutual funds pay out their capital gains to shareholders. While generally speaking, a capital gain means an investor made money on an investment this is not always the case with those who hold mutual funds.

Some of the potential benefits of mutual funds, (ie. owning a diversified, professionally managed portfolio) may sometimes result in some unintended consequences, like capital gains. Because mutual fund portfolio managers are actively buying and selling throughout the year and owners investment dollars are pooled with that of other investors with different holding periods, the funds are allowed to pay out all of their capital gains to all current shareholders on a specific date, (typically in December). This means that an investor that just purchased the fund last week in their taxable account, could end up paying taxes on a capital gains distribution even though the value of their investment is currently flat or underwater. In essence, many mutual fund investors end up paying taxes on gains even though they were not along to enjoy the ride.

Let’s examine a scenario showing how this could unfold in a hypothetical investor’s account. Art Vandelay has decided he wants to diversify some of his personal funds outside of his importing/exporting business by investing $100,000 in his taxable brokerage account into the ABC Flagship Mutual Fund. When he purchases shares in the mutual fund on December 10th, they are valued at $10.00/share and he is able to buy 10,000 shares. Due to some highly appreciated securities that were sold within the fund earlier that year, the fund is paying out 10% of its value in the form of a capital gain on December 15th. At the market close on the 15th and assuming no change in the market value over the 5 days since his original purchase, Art will have 10,000 shares of the fund valued at $9.00/share. On the following day, a capital gain of $1.00 per share will be paid back into his account for a total of $10,000 (often this is just reinvested back into the fund). Now while Art’s portfolio value is still no larger on the 15th than what is was on the 10th, he will owe Uncle Sam taxes on this capital gain payment of $10,000 at his capital gains rate of 15%. This would be quite discouraging for Art to pay $1500 in taxes even though he has yet to make a profit on his investment!

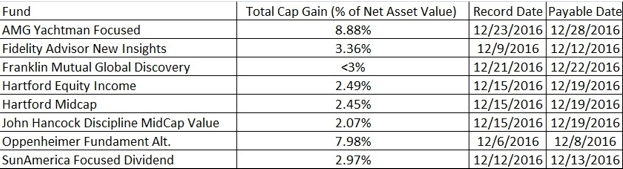

Below are some of the funds expected to pay capital gains greater than 1% and the projected amount:

What to do now?

Because of this potential tax trap, we believe it is important to review your current tax situation and portfolio with you prior to year end. If you are getting cash to work, it also may be advantageous to purchase funds that are paying out large gains after their payable date by waiting an extra day or two. It is also important to note, that while this doesn’t impact the taxation of mutual funds held inside of retirement accounts like IRA’s and Roth IRA’s, some clients may notice that the value of their accounts will show a large fluctuation the day prior to the capital gain being paid into their account as the funds share price drops by an amount equal to the capital gain being paid out. This is more noticeable in years when many funds are paying out large capital gains.

For many clients we have been shifting to passive models invested in index-based funds that typically have lower turnover and may be subject to lower capital gains. If you are in a higher tax bracket and have significant funds invested outside of retirement accounts, reviewing this may be warranted. For more on the pros and cons of passive and active investing refer to Is Warren Buffett Giving Contradictory Advice?

From a pure investment perspective, there are many potential benefits to owning mutual funds including having a diversified, professionally managed portfolio as well as the ease to which they can be purchased. Just as with any financial matter though, it is important to consider the impact of ownership from multiple angles including taxation. Before making any investment in a mutual fund, you should review the fund’s prospectus as well as consult with a qualified financial professional to examine the ramifications to your overall situation. We also encourage you to visit Morningstar.com to learn more.

Nick Hughes is a Wealth Advisor with Franklin Wealth Management, a registered investment advisory firm in Hixson, Tennessee. In addition to advising clients since 2007, he has contributed to articles for Market Watch and FinancialPlanning.com and is a regular contributor to the Franklin Backstage Pass blog.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.