What a Difference a Year Makes!

Those who thought the S&P 500 would be the best place to invest in 2016 may have been surprised to find that “the beef” was to be found in many other types of investments last year. Some of the most unloved asset classes recovered well after February with Energy, Commodities, Emerging Markets and Smaller U.S. Companies all outperforming.

Last year we wrote a story concerning a farmer that raised dairy cows who grew concerned about his herd growing skinny even though milk production was increasing. We related how this was akin to income oriented stocks experiencing one of the worst years in recent history even though the dividend payout was either holding steady or increasing. Most companies not named Facebook, Google, Amazon or Netflix suffered in 2015 and smaller companies lagged larger ones.

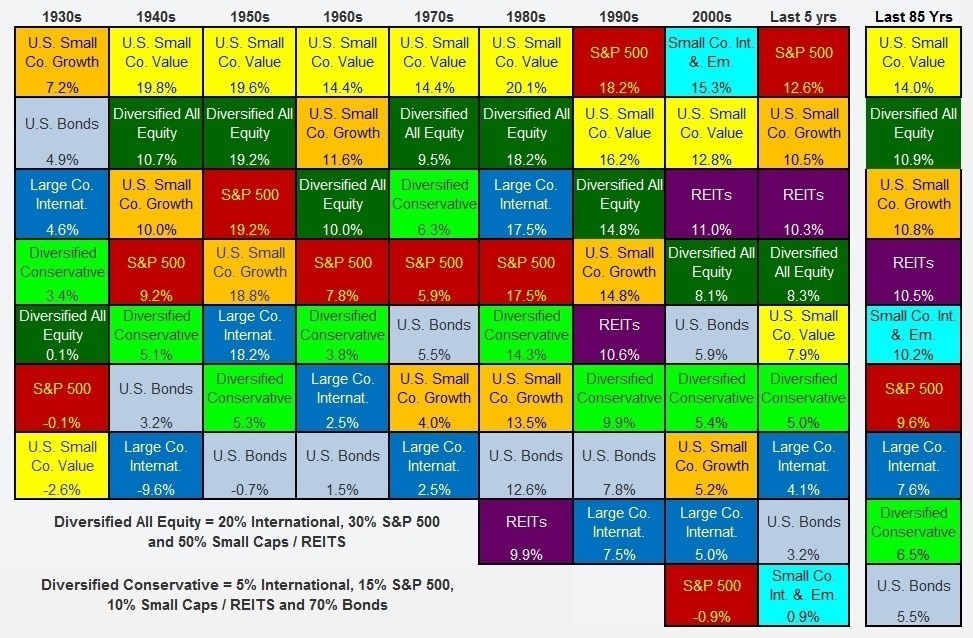

In 2016, smaller companies and dividend payers fared much better than in the previous three years when it seemed all the gains belonged solely to large company U.S. investors. Those “Skinny Cows” that many were worried about have recovered well and outpaced most other investments over the last year. Investors who maintained diversified portfolios were rewarded this past year by their exposure to smaller companies and to developing markets to a lesser extent. The past year was more of a return to normalcy as most U.S. holdings increased in value, but the smallest recovered more. As can be seen on the chart below, over an 85 year period through mid-2015, smaller companies have outperformed by a wide margin.

We continue to maintain that our diversification in smaller, lesser known companies, dividend growers and holdings outside the U.S. will lead to more long term consistency and a more-steady ride through the years. There will be periods like the end of the 1990s and the last few years prior to 2016 when it seems that diversification is no longer a good strategy. For those who doubt the wisdom in maintaining investments outside the largest U.S. companies, just talk to those who “un-diversified” in the early 2000s or consult the chart below.

Investors Rewarded for Holding Steady

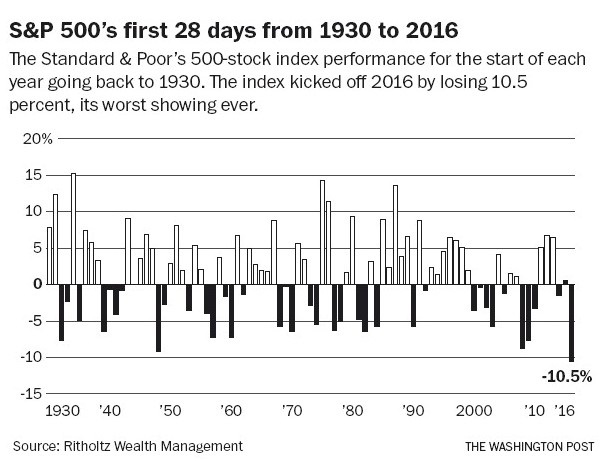

“As goes January, so goes the year.” That was the refrain when 2016 began with the worst start ever. Following a lackluster 2015, the Standard & Poor’s 500-stock index fell 10.5 percent over the first 28 days. The narrative at the time was all over the place: Stocks fell because of the imminent China collapse, or an earnings recession, or election uncertainty, or (my personal favorite) “this bull market is long in the tooth.” These are all examples of the “narrative fallacy” — the attempt to make sense of something after it occurred, ignoring the facts that don’t fit a convenient story line.

There were plenty of calls to SELL EVERYTHING in January and February.

That is rarely good advice; it was especially bad advice in the first quarter of 2016. Had you sold in January, you would have missed a 45 percent rise in small-cap stocks, a 36 percent gain in Japan, 25 percent gain in U.S. large-cap stocks, 31 percent gain in emerging markets, and a whopping 57 percent gain in energy-related stocks (We had increased our energy exposure in the last quarter of 2015, just a couple of months too soon). Missing rallies of this nature can be devastating to the long-term performance of any portfolio.

What about valuations?

By just about every single valuation metric, the United States is more expensive than Europe or Japan or emerging markets (pretty much in that order).

Let’s start with CAPE — the cyclically adjusted price-to-earnings ratio. Think of it as the 10-year P/E ratio. It is high for U.S. equities by historical averages, elevated for Japan, moderate for Europe and low for emerging markets.

Since 1990, the S&P 500 has traded above the average CAPE ratio in 307 of 324 months — that’s 95 percent of the time. If you abandoned U.S. equities when the CAPE ratio was overvalued, you would have missed gains of more than a 1,000 percent over that time. In fact, had you only invested when the CAPE was 25 percent overvalued — i.e., when stocks were simply “expensive” — your total returns since 1990 would have been 650 percent. This is one of many reasons it is ill-advised to use valuation as a timing mechanism. One can use these figures as a reason to ratchet down expectations, but not as a reason to avoid investing altogether.

New Developments for 2017

Many of you who subscribe to Kiplinger have been asking about how the new Fiduciary rule is going to impact the way we interact with clients. For the most part we see these changes as a great development for investors. Unfortunately, it may add additional paperwork for some and additional regulations for many.

Kiplinger Article: 8 Things You Must Know About the New Broker Rule

Anyone advising investors on any type of retirement plan is now required to act as a fiduciary, which means we are required to put the client’s interest first. Certified Financial Planners were already required to adhere to this standard but now everyone is required to no longer just recommend what is suitable. We need to know enough about our clients and have the expertise to know what is best for our clients.

Simplicity and Savings

Most of our clients already work with us on a non-commission basis. For those few who do not, we may want to look at our options before the April 2017 deadline.

For all that we work with on a non-commission basis, we have been able to work with LPL to improve things in several ways:

1) We have been able to negotiate the elimination of transaction charges in client accounts.

2) We can now buy funds and ETFs with lower internal expenses without being concerned about additional costs.

3) We can now include all accounts in automatically figuring tiered schedules, reducing costs automatically when new levels are achieved.

4) We can also more easily utilize flexible billing so that those who itemize their deductions can save additional tax dollars.

In the next couple of months we can go through these updates in detail on a one on one basis. We should be able to detail how internal expenses can now be reduced for all core strategies and detail the economics of these improvements.

We continue to believe that clients should primarily adhere to core strategies and consider other strategies to add diversification:

A few firms are in the process of implementing sweeping changes for all clients that limits flexibility somewhat. We still want to allow flexibility for our clients if they wish to own specific types of products. We believe the changes will finally force some hidden fees into the forefront and most clients will be better off.

Our New Holding Company

Over time our company has grown to include more offices in varied locations. We recently created a holding company so that these offices can maintain their identity and we can focus on making sure they have the systems, technology and support to help them the best we can. This holding company is named Innovative Advisory Partners L.L.C. and encompasses our three partner companies, Franklin Wealth Management (North of the River), Solomon Wood Financial Advisors (on Broad Street) and Bridgetown Investment Council (on Signal Mtn.). Statements for those who work with us on a non-commission basis will show this new holding company as we go through the process of updating the accounts to eliminate ongoing transaction charges.

Rules and Systems to Eliminate Biases

We have found over time that investors’ emotions cause them to be their own worst enemies when it comes to making smart investment decisions over time. To the extent we listen to the media or allow our fears or greed to get the best of us, we hamper our results and shortchange ourselves. Some of us chase what has done the best recently, while others avoid mathematically superior options because of unfounded fears. Others, like myself at times, believe we are smarter and not subject to these biases.

We created a test to help determine what biases each of us are most predisposed toward. We unveiled this test at our Brain Games workshop last year and realized it needed a bit of work to simplify the process.

The easiest way to avoid being thwarted by our own emotions is to establish investment rules and automate these as much as possible. Quantitative criteria are easier to automate. Qualitative criteria will always need to be considered as well, and we will be successful to the extent we are able to follow our guidelines and rules, provided they are well researched and thought out.

Below are our 8 primary criteria for holdings in our MF Models. It is worthy to note that we will always maintain diversification and never chase the most popular index in these MF Models.

- Long term track record showing outperformance with the same portfolio manager. They should show outperformance since inception or the last 10 years relative to their benchmarks.

- Minimization of downside risk. All holdings are ranked based upon downside risk measures and graded to optimize the portfolio model.

- The most consistent MF holdings are chosen over those less consistent. These rankings are based upon year to year and trailing four year periods over long time horizons (up to 20 years). Inclusion in the MF models is dependent upon exceeding the averages at least 50% of the time and in most cases much more often for both 1 year and four year trailing periods.

- Expense ratios for each holding relative to its category should be better than average. We place more importance on the first three criteria than the fourth, valuing quality over cheapness.

- We look for high manager ownership. Portfolio managers should eat their own cooking.

- We prefer those managers who are not afraid to concentrate their holdings into their highest conviction ideas.

- We prefer managers who have shown that they think differently from the crowd (to the extent of being contrarian at times). Those who are able to do this and maintain the right temperament do well over the long run.

- We prefer to work with representatives who are communicative and let us know first when anything concerning may have transpired within one of our MF holdings.

We should be expounding upon these rules for equity investments in our Stock and ETF models in later writings.

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, and CEO of Innovative Advisory Partners, a registered investment advisory firm in Hixson, Tennessee. A 20+year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.