For decades, the traditional retirement strategy was relatively straightforward. Work hard, save consistently, pay off your home, and retire comfortably. Today, that strategy is being challenged.

Higher inflation, rising insurance costs, elevated interest rates, and increased living expenses have forced many retirees to reconsider their plans. Some are delaying retirement, and other are returning to work. Many are simply looking for ways to make their retirement dollars stretch further.

At Franklin Wealth Management, we’ve spent years helping families navigate retirement. While every situation is unique, we’ve noticed that the retirees who thrive often focus less on chasing investment returns and more on building a sustainable lifestyle.

Here are seven retirement strategies worth considering in today’s environment.

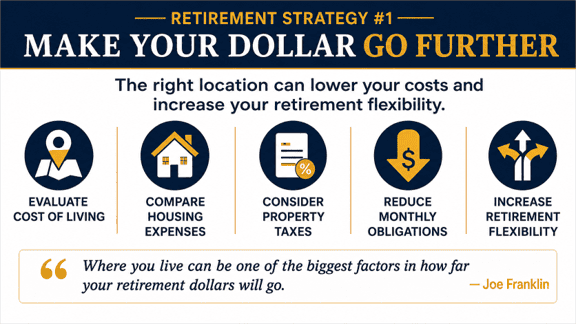

1. Moving to Cut Costs

One of the most powerful financial decisions retirees can make isn’t selecting an investment—it’s deciding where they live. Many retirees find that relocating to a lower-cost area allows them to maintain the same lifestyle while significantly reducing housing, property tax, insurance, and everyday living expenses. For some families, this may even create flexibility to spend part of the year near children or grandchildren while maintaining a more affordable primary residence.

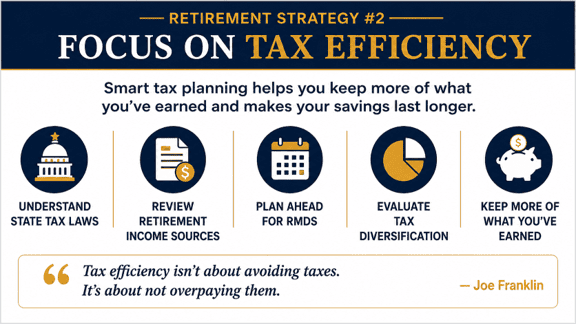

2. Don’t Ignore Tax Efficiency

Retirement isn’t just about how much money you’ve accumulated. It’s also about how much you get to keep. Different states have different tax treatments for retirees. Depending on your circumstances, factors such as state income taxes, retirement income taxation, and investment income treatment can significantly impact your retirement cash flow. Tax planning often becomes especially important during the years between retirement and when Social Security or required minimum distributions begin.

3. Good Debt vs. Bad Debt

Few things create peace of mind like entering retirement with minimal debt obligations. For many retirees, reducing or eliminating debt can lower financial stress and provide greater flexibility during market volatility. Every situation is different, and decisions involving mortgages or other debts should be evaluated carefully. However, reducing high-interest debt often remains one of the most impactful steps retirees can take.

Additionally, debt may be your friend in an inflationary environment. If you happen to have debt with very low interest rates and an asset that can accumulate value over time, you may want to consider hanging onto this debt during times of inflation. In short, if the government wants to inflate away its debt, you may want to take advantage of this as well.

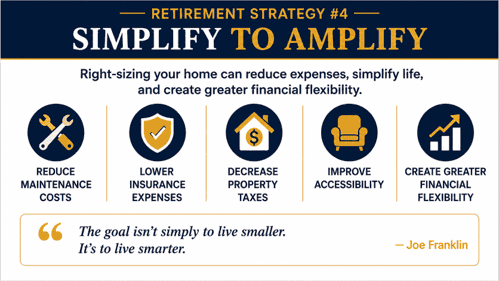

4. Too Much of THIS Could Be a Bad Thing

At one stage of life, a larger home may have made perfect sense. In retirement, that same home may create unnecessary expenses through maintenance, insurance, taxes, utilities, and upkeep. For some retirees, downsizing can free up cash flow, simplify life, and better align their living environment with future needs. The goal isn’t necessarily to live smaller. It’s to live smarter.

5. Sell These Things Before You Retire

Retirement often provides an opportunity to evaluate possessions and expenses accumulated over decades. Boats, recreational vehicles, extra vehicles, and other lifestyle assets can create ongoing maintenance costs that may no longer align with retirement priorities. Simplifying doesn’t mean sacrificing enjoyment. It means being intentional about what truly adds value to your life.

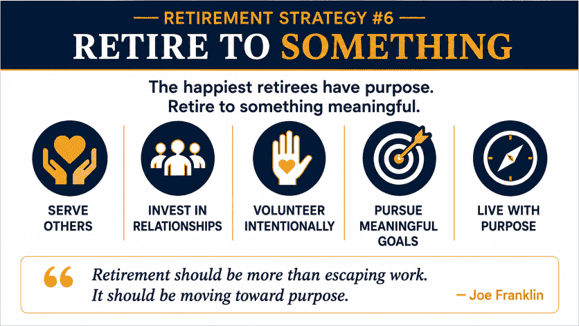

6. The Cure for the “Go-Go” Hangover

Many retirees spend years planning financially for retirement but very little time planning emotionally for retirement. The happiest retirees often have something meaningful to pursue—whether that’s family, volunteering, ministry, mentoring, travel, hobbies, or community involvement. Retirement should be more than escaping work. It should be moving toward purpose. For those of us guided by faith, retirement can become an opportunity to deepen our impact and invest our time where it matters most.

7. Extend Your 700 Weeks

Perhaps the most valuable retirement asset isn’t your portfolio—it’s your health. Many studies suggest that maintaining physical activity, healthy nutrition, and strong social connections can contribute to a better quality of life throughout retirement. The objective isn’t simply to add years to life. It’s to add life to your years. When you prioritize your health, you create more opportunities to enjoy family, travel, hobbies, and meaningful experiences throughout retirement.

Final Thoughts

The retirement landscape continues to evolve, but the fundamentals remain remarkably consistent. Retirees who focus on controlling expenses, reducing debt, managing taxes, maintaining their health, and living with purpose often place themselves in a stronger position regardless of economic conditions. The goal isn’t simply to retire. The goal is to retire well.

If you’d like more retirement planning insights, subscribe to The Mustard Seed YouTube channel and follow Franklin Wealth Management for educational content designed to help families make informed financial decisions.