WALL STREET’S PIGS AND WOLVES

Brokerage firms are finding many stealthy ways to market proprietary products and strategies these days. We wrote about some of these conflicts of interest in our blog a few weeks back entitled Wall Street’s Pigs and Wolves.

There are many good advisors at brokerage firms that are primarily focused on providing good advice for their clients. Many of these good ones are feeling the pull to be more independent and fully embrace what is known as the fiduciary standard in their dealings with clients. The inherent conflicts of interest exist primarily to increase the profits of their firms at the expense of their clients which flies in the face of what many good advisors are trying to provide in the form of client centered advice.

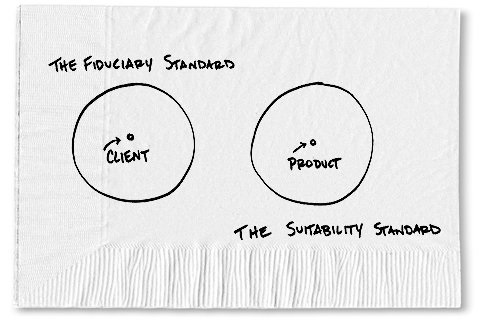

A DIFFERENCE IN STANDARDS

The key difference in the advice provided can be boiled down to the standards employed by a broker at a typical brokerage company and a Registered Investment Advisor. A broker can recommend most anything, including proprietary products manufactured by their firm to his or her clients as long as they are suitable or not too risky for the client. If fund A has had more stable and greater long term returns than fund B, many times fund B is still recommended because it may provide higher compensation for the broker. Many relatively good firms do not provide any more compensation for one product over another product, but the political pressure is still there to funnel business into particular fund families or programs. If a broker recommends a particular strategy or program managed at the broker’s home office, it may signify that they are doing something that is not necessarily in your best interest. If you own one or two proprietary funds or managed asset programs, this is not always a bad thing just as if someone drinks alcohol, it does not necessarily mean that they are an alcoholic. The key determinant is how much of your portfolio is in proprietary products or how much and often someone drinks alcohol. Moderation is definitely preferred.

In contrast, a fiduciary is required to do what is in the client’s best interest. If one product or strategy is clearly better than another, this should be the product or strategy recommended. The best way to eliminate these conflicts of interest of course is to eliminate proprietary products or strategies. As we have stated before, you are much less likely to eat junk food if you keep it out of the pantry. I would say that many proprietary funds offered by these banks and brokerage firms may be good ones. In our practice we will occasionally use one of these other firms’ proprietary firm’s products or strategies if we feel it is what is best for the client. Our motivation to recommend one investment over another can be based more squarely on the needs of our clients because we are independent.

To see a good video on the difference between a Registered Investment Advisor and a Broker, click on the image below.

Earlier this year, J.P. Morgan had unfortunately been saddled with quite a bit of negative press regarding conflicts of interest. Another article was published today on yet another blemish with regard to proprietary products (see below). These types of practices generally seem to happen less today than in years past. Today what is typically recommended involves the firm managing a proprietary strategy that may or may not contain funds that they also manage.

http://online.wsj.com/articles/j-p-morgan-faces-more-questions-on-conflicts-of-interest-1407514915

We do not necessarily want to focus only on JP Morgan with regard to this. They have just been in the news a lot more lately.

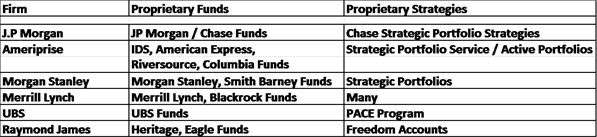

The following firms provide or used to provide the accompanying funds and strategies. This is an incomplete list, but contains some of what we currently see when reviewing statements provided to us by those referred to our practice. If a portfolio is overly concentrated with these proprietary funds or strategies, this could be cause for concern.

THE MARKETS

So far this year, an individual invested in bonds has generally done better than those invested in stocks. This market has been going nowhere all year. We’re still looking for value but, like Warren Buffet, we would prefer to wait until the fat pitch at this point instead of trying to swing at the junk pitches that Mr. Market is throwing.

Warren Buffett notoriously waits for the “fat pitch” — and now, all this waiting has led to a huge amount of cash.

According to Bloomberg News, Warren Buffett’s Berkshire Hathaway Inc. “cash rose past $50 billion at the end of June,” which is the first time “it finished a quarter above that level since he became chairman and chief executive officer more than four decades ago.”

The amount of $50 billion is more than twice that which Buffett likes to “keep on hand should his insurance businesses have to pay unusually large claims.”

But “the guy’s just not going to spend the cash to spend it,” according to David Rolfe, Wedgewood Partners’ chief investment officer who was quoted in the Bloomberg article.

Typically, Warren Buffett’s investment strategy is to wait for the fat pitch. For those unfamiliar with the term, a “fat pitch” is the “opportunity to buy a company at a price promising favorable returns.”

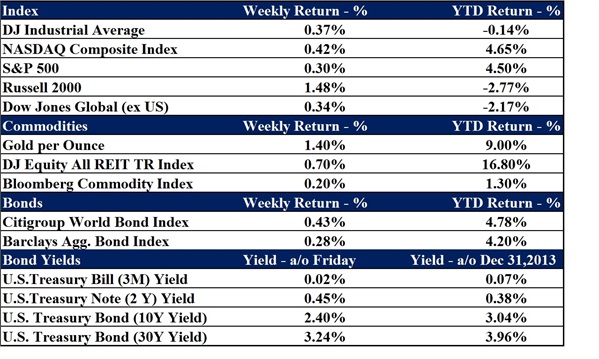

Data as of 8/11/14

Data as of 8/11/14

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are un-managed and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.