The 2018 Tax Cuts Are Set to Sunset in Two Years. What are you doing about it?

Feeding the Goose that Lays the Golden EggsIt has been a little over a month since I sent my obligatory check to Uncle Sam so that we may continue to enjoy the freedoms this country provides. Our ancestors fought and died for these freedoms and our tax dollars, spent well, may help preserve these freedoms. We like to be able to feed the goose that lays the golden eggs, but what if the goose requires us to feed it more and more and grows too fat and bloated to produce the eggs she once provided? It seems that as our population becomes more mobile, many citizens are voting with their feet and choosing to live in areas with lower taxes, lower costs, and better climates. Almost every week, we meet someone who has recently moved here from Illinois, New England, or California. Tennessee is not as popular as Florida, but it’s where many are choosing to relocate. Tennessee currently has no income taxes or estate taxes, and our citizens can buy larger homes and enjoy a lower cost of living than in many other states. We cannot avoid a lot of federal taxes the way some do by relocating to Puerto Rico, but we also don’t have to worry about as many travel restrictions either. While Franklin Wealth does not intend to start preparing taxes, we want to make sure that we are saving clients as much as we can by reviewing tax documents and planning for the future. It is likely that taxes will revert to the Obama Era tax rates in 2025, and we want to prepare for this change by looking to reduce taxes now and in the future. In the last few weeks, we have been teaching classes on “Taxes in Retirement” and highlighting many of the changes in the Secure Act 2.0 that were passed in the last-minute spending bill for the 2022 Congress. How much may Taxes Increase?The 2018 Tax Cuts and Jobs Act (TCJA) created many tax changes for both corporations and individuals. Many of the biggest individual changes were written to expire after the 2025 tax year. These sunsetting tax provisions create additional complexity in an already complex tax planning environment. Barring any extension of the 2018 TCJA tax rates or a new tax bill being signed into law, there are two big items we can plan for before the 2025 sunset. |

|

|

Roth ConversionsA Roth conversion is a tax strategy to convert pre-tax retirement funds, such as those in a traditional IRA, to a Roth IRA by paying taxes on the converted amount, ideally at a lower rate than you would in the future. Once the funds are in the Roth IRA, they’ll continue growing, and withdrawals are tax exempt once you reach age 59 ½ and the account is at least five years old. An easy way to think about it is that the IRS is running a sale on Roth conversions for the next two years. Each year that passes, you’re losing an opportunity to save on converting some of your pre-tax money to a Roth at the lower rates. For example, a married couple with taxable income of $83,550 is at the top of the 12% bracket. If they complete a Roth conversion of $256,550 to max the 24% bracket, they will save $15,651 in federal taxes by performing the conversion in the next two years instead of waiting until after 2025. That’s $15,651 that will stay in their pocket and grow tax free! |

|

|

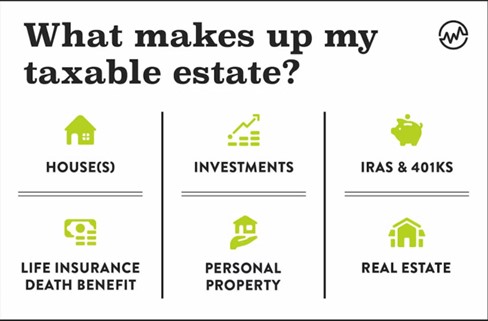

Estate Tax ExemptionIf you have a sizeable estate, another large opportunity to take advantage of before the 2025 sunset is the increased estate and gift tax exemption amount. The exemption amount will be cut in half for each taxpayer and is estimated to be around $6.2 million in 2026 after adjusting for inflation. This change will not only affect estates over the current exemption amount of $12.06 million but also those in the $6-$12 million range, as these estates will suddenly find themselves subject to taxation. Making lifetime gifts now to take advantage of the increased exemption amounts will remove not only your assets from estate taxation but also any appreciation on said assets. The IRS has issued regulations to prevent a clawback on your lifetime gifts made during the increased exemption period. The regulations allow you to make gifts over the lower 2026 exemption amount and up to the current exemption amount without worry that your estate will claw back the excess exemption used. Your estate would be granted an exemption amount up to the amount of excess exemption used. For example, if you make lifetime gifts of $8 million in 2022 and pass away in 2026 when the exemption amount has reverted to $6.2 million, your estate will get the benefit of the estate tax exemption of $8 million and not just the $6.2 million. However, an important caveat is if you gift less than the estate exemption amount in effect at your death, you will receive no benefit. In other words, if you gift less than $6.2 million before 2026, your estate will receive no additional exemption amount over the current exemption upon your death. The current increased exemption is a use it or lose it benefit if you have a large estate and live past the 2025 sunset. In some good news, portability elections made during the increased exemption period will not be affected by the sunsetting provision. The full increased exemption amount transferred to the surviving spouse will be available for their estate after 2026. |

|

|

Deferring Capital GainsWe started utilizing Opportunity Zone funds to defer a relatively substantial amount of capital gains for clients in 2021. This was a year when portfolio adjustments, business sales, and property gains put clients in a position to owe more taxes than in most recent years. While we are typically able to identify areas within portfolios to sell securities to realize short-term losses as an option to offset these gains, in November and early December of 2021, we had a hard time finding anything to sell at a loss come year-end. However, we were able to research and position clients into publicly traded and liquid Opportunity Zone funds to keep from paying as much in capital gain taxes for that tax year. We were able to sell the Opportunity Zone funds at a minimal gain in 2022 and either defer the taxable gains or even completely eliminate them for some. A few clients still own these Opportunity Zones to continue deferring taxes, but for many, they only had to hold these for a month or two to keep the taxes down. These holding periods differ for each person, but it is conceivable that these investments only be held for a week or two to push tax payments back a year or completely eliminate the taxes in the best-case scenarios. Those with significant capital gains in 2023 can also utilize these as long as they find and invest the gains in Opportunity Zone properties or the funds within six (6) months. The capital gains hit can be reduced from the highest tax bracket (for short-term gains) to the long-term capital gain rate of 15% to 20%. Those in the 20% capital gains bracket can sell the Opportunity Zone investments over time to reduce the tax rate to 15%. Those who are not showing much taxable income could conceivably spread the capital gains enough to reduce the long-term capital gain rate to zero. |

|

|

| For clients with portfolios which are dominated by company stock, diversification is often beneficial but may be costly from a tax standpoint. If someone has over 50% of their portfolio in one stock, sometimes this pays off well. Those who worked for some of the biggest and most popular companies in the late 1990s felt their company could do no wrong; but if they worked for companies like Worldcom or Enron, their futures were decimated in the early part of the next decade. Others who worked for companies like GE saw their net worths dissipate more slowly. In general, those working for the biggest and most popular companies did not fare as well as the market as a whole. |

|

|

To avoid these types of scenarios, individuals may choose to consider exchange funds. Exchange funds allow investors to exchange shares with significant potential tax liabilities from gains built up over a period of years for a portfolio which is more similar to the S&P index. Most larger U.S. companies can be exchanged for shares in these exchange funds. These portfolios then become more diversified, rather than being dominated by one stock. At the same time, these investors reduce the risks associated with owning stock in predominantly one company and their taxes can continue to be deferred until they sell the funds.

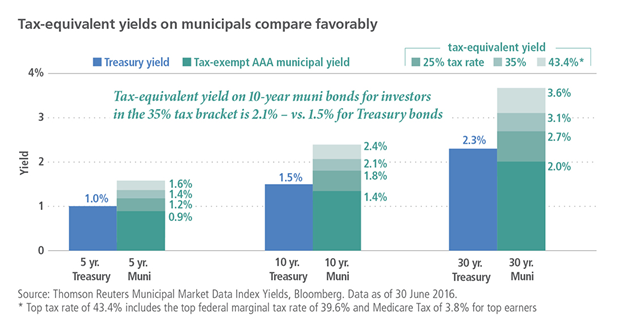

Review Your Tax ReturnsWe have noticed that some tax preparers are failing to adequately utilize the Opportunity Zone capital gain tax deferrals available and may not be carrying forward capital gains debits to save taxes on future tax returns. We have noticed these oversights by reviewing schedules and using our tax analysis software to catch easy misses. This software enables us to objectively analyze tax returns and determine whether improved tax strategies may be beneficial.Investors have become more concerned about a possible recession and are noticing that they can reduce the risk in their portfolios while still getting over 5% in CDs, treasuries and some tax-free bonds. Restructuring these portfolios may come at a cost in the form of taxes, however. For those in higher tax brackets, municipal bonds make a lot of sense, although they don’t pay quite as much interest. Fortunately, investors do not pay taxes on the interest. A 4% tax-free bond pays the equivalent of 6.5% for someone in the highest tax bracket. It is beneficial to consider what taxable vs. tax-free bonds are paying, especially considering that longer term treasuries tend to perform best out of all types of bonds (and investments in general) during recessionary periods. |

|

|

Being Charitable while Avoiding Capital Gains TaxesSome investors may want to give to their church or favorite charity and feel they have some stocks that are currently over-valued. If they sell these stocks, they have to pay taxes on their gains, but if they give these stocks directly to their church or charity, they can avoid paying these taxes. These entities are also exempt from taxes, enabling them to pay nothing to the government as well. Charitable Trusts can also create significant tax savings for those who wish to pursue this option. If set up correctly, capital gains taxes can be avoided, federal income tax deductions become available and additional tax benefits are available to donors in the early years. These trusts can be set up with income for life to multiple beneficiaries with the remainder being donated to charity in the form of a Charitable Remainder Trust. Conversely gifts can also be made for a specified period to charities with the remainder to multiple beneficiaries. These trusts have become more popular since Congress eliminated the stretch IRA for non-spousal beneficiaries as they can also allow for distributions over a period of more than 10 years rather than forcing beneficiaries to liquidate all holdings by the end of the tenth year. |

Other ChangesThere will be numerous other changes to tax provisions once the 2018 tax law has fully sunset. Itemized Deductions

The options listed above are some of the ways taxes can be potentially reduced, deferred or eliminated in the short-run for taxable portfolios. Structuring portfolios to be more tax efficient over the long-run may take more time, but it typically proves to be more beneficial. We have found that the taxes saved by going through our tax planning process is often much more impactful than making an extra percent or two on portfolios. |

|

Forbes Recognized Joe Franklin as one of the Top Advisors in Tennessee |

|

4700 Hixson Pike Hixson, TN 37343(423) 870 – 2140www.Franklin-Wealth.com |