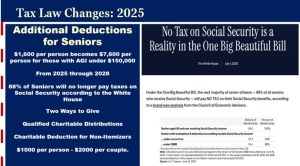

When the new tax laws were passed through the Big Beautiful Bill in July, we recognized that not everyone would be able to benefit from having “No Tax on Social Security”. The promise was that anyone making under $150,000 would be able to avoid these taxes, but not those making above this amount. For the last couple of months, we have been dissecting what new benefits clients will have and how to best plan for the new “Senior Deduction” during the next four years through the sunset of this deduction in 2028. It may be that some may still benefit from taking Social Security sooner, but others with higher incomes may wish to defer income for longer so that they do not lose benefits.

It seems that just about everyone’s income tax will be coming down some, but those in lower tax brackets stand to benefit more under the new rules.

How do the New 2025 Tax Law Changes Affect Social Security?

Most people under the age of 61 will be unaffected by the new Senior Deduction. Certainly, if both you and your spouse are under the age of 61, neither of you will be able to utilize this (unless extended) as it sunsets at the end of 2028. But for those who are old enough to utilize this deduction (if you are 65 or older by the end of 2028), we want to see how we can best plan to get maximum benefits.

Starting this year, the standard deduction will be $31,500 for a married couple. Those over 65 will also receive the current senior benefit of $1600 per individual, plus an additional benefit of $6000 per individual through the new tax law. The current administration estimates that 88% of all those currently receiving Social Security will no longer have to pay taxes due to this new additional deduction.

In addition, those who give to a church or charity can deduct $1000 per person ($2000 for a couple) in addition to the standard deduction. For those over 65 who choose to give at least $2000 to a church or charity, the total deductible amount is now $48,700. Anyone showing income of less than this amount will pay no taxes, and someone with solely Social Security income of less than $97,400 will also not have to pay any taxes between now and the end of 2028.

More on the Senior Deduction and how it affects Social Security (especially for couples) can be found by clicking the video link ABOVE.

The Social Security Tax Loophole

Over the next four years, it may prove even more beneficial to plan out when you want to draw Social Security, how much you may want to be drawing from retirement to live on, and how much you may want to convert to Roth IRAs to minimize taxes in the future.

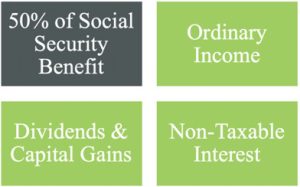

Many are unaware of how Social Security is taxed or how to reduce the taxation on these benefits. The formula is not intuitive but is relatively easy to figure out. All of your taxable income (outside of Social Security) is included in the calculation, plus tax-free interest, plus one-half of your Social Security income.

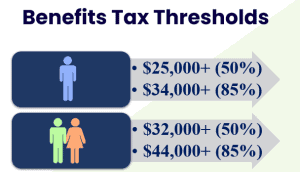

The income thresholds are shown below. If the calculated “provisional income” is below the first threshold ($25,000 for singles and $32,000 for couples), then there is no tax on the social security. Social Security income above the first threshold is taxed at 50% and income above the second threshold is taxed at 85%.

Taxes on Early Social Security Versus Waiting Until 70

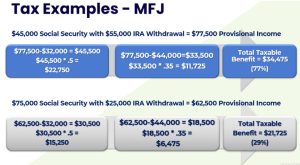

Let’s assume a couple has expenses of approximately $8,000 a month and wants to live on $100,000 a year from Social Security and IRA distributions. If they start taking Social Security as soon as possible at 62, the benefit amount would be $45,000 in this example. Provisional Income would be the entire amount of the IRA withdrawal and one-half of the Social Security benefit.

In this case, one-half of the Social Security income is $22,500, so the provisional income is $77,500 after we add in the IRA withdrawals. The amount of Social Security that is taxed at 50% would be the amount over $32,000 or $22,750. The amount over $44,000 would be taxed at 85% which equates to an additional 35% on top of the 50%. Subtracting $44,000 from the total leaves $33,500 taxed at an additional 35% which means we have to pay taxes on an additional $11,725 in Social Security. So when we add these two numbers together, we arrive at $34,475, which is the total amount of Social Security that is taxed (This is 77% of the total).

If we wait, we do not have to draw as much out of our IRA to make up the difference after the age of 70. The “provisional income” is lower because there is more Social Security that we only have to count at 50% in the calculation to make up the entire $100,000 a year in spending.

With a provisional Income amount of $62,500, the amount taxed at 85% is less, and the total taxable benefit is only $21,725 versus $34,475 when drawing at age 62. Furthermore, the total taxable benefit is only 29% of the $75,000 in annual Social Security, versus 77% in the first scenario. This social security amount can continue to grow, indexed for inflation, and a greater amount will be left for the surviving spouse as well.

When we figure the amount that is subject to taxation after all the deductions, we want to consider the taxes prior to and after the sunset of the Senior Deduction. Delaying Social Security may enable more of this deduction to be utilized prior to the sunset and also allow for less Social Security to be taxed.

The Best Way to Reduce or Eliminate Social Security Taxation

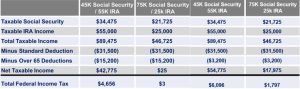

When we consider “provisional” social security income that is taxed, the formula includes tax-free interest but does not include tax-free distributions. If most or all additional income outside of Social Security is in the form of tax-free distributions, then we will have even less of our Social Security taxed. In the example above, let’s assume that prior to age 70, the couple was able to convert their entire IRA to a Roth IRA over the course of 8 years, and instead of withdrawing $25,000 out of the IRA, they are taking from a Roth IRA.

Provisional Income would only include half of the $75,000 Social Security amount, or $37,500. Of this, only 50% of the amount over $32,000 would be taxable. This means that the taxable social security would be $2,750, and the Roth IRA Income would be ZERO. Even if Senior Deductions are eliminated and the Standard Deduction gets cut in half as it was scheduled to prior to the “Big Beautiful Bill”, inflation could allow for the Social Security benefit to grow to over $110,940 before any tax would be necessary (In this case, we are assuming a reduced deduction amount of $15,750).

Of course, choosing when to draw Social Security, how much in IRA distributions to take, and what the optimal amount of Roth Conversions to make are all dependent on many variables and are different for each individual or couple.

A Simple Scenario

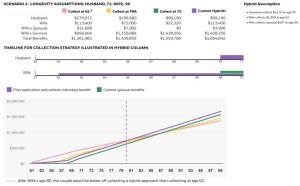

Looking at a scenario based upon just one or two variables can be beneficial to understand what may be best if we do this prior to looking at the whole landscape of options. In the case below, we are just considering ages and benefits at different ages for a couple. Many times, the best option is different if one spouse passes early, as we are showing below.

In this case, we are looking at the husband passing at 71 and the wife living to 99. The least amount of benefits will be provided if they both draw at 62, assuming we have no outside investments and we are only considering Social Security benefits. If they both wait as late as possible to draw, they will get more over their combined lifetimes than if drawing at full retirement age or at 62, as well.

The maximum amount of benefits are provided in this case when the wife draws as soon as possible, the husband waits until age 70 to draw, and the wife switches over to her husband’s survivor benefits after he passes away at age 71. Considering the average age of widowhood in America today is now 59 years of age, it may be best to look at more assumptions with the husband passing away sooner. We want to expect the best but plan for the worst.

What if the Wife is Still Working?

Eligibility for Social Security requires a minimum of 10 years of work. Furthermore, if someone has only worked for 30 years and Social Security is taking the average earnings for the highest 35 years, many will want to put in the extra 5 years to get a higher benefit. If we want to start drawing at 62, but we are still working to get our 35 years in and get a higher benefit, Social Security will penalize us if we earn over $23,400 in any of these years before our Full Retirement Age (67 for anyone who is 62 or younger today).

If we earn $43,400, we will have to pay back half of the amount over $23,400, which equates to $10,000. Most don’t like the idea of having to pay these penalties.

If we decide we are not going to work any longer, but someone gives us an opportunity we cannot refuse prior to our Full Retirement Age, we cannot fix the situation if we are trying to do this and it has been over a year since we started drawing. We are still forced to pay the penalties. We want to be pretty certain that we are not going to be working and earning much more than $23,400 after we start drawing our benefits.

What if the Husband has Already Passed Away?

Survivor benefits are also subject to these penalties. These can be received as early as 60, but you still want to be absolutely sure you will not be working and earning more than $23,400 if you are drawing a benefit prior to your Full Retirement Age.

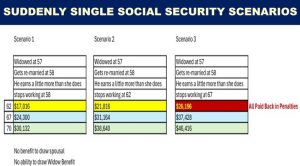

Three Scenarios are shown above. In each of these cases, the husband passes when the widow is 57, and she gets remarried at 58. Getting remarried, unfortunately, invalidates her survivor benefit, but there is nothing she can do unless her new husband also passes away. If he were to pass away, she could choose between the survivor benefits of her two husbands.

In these scenarios above, we show her quitting work after 25 years, 30 years, and 35 years of working. Stopping work at 62 allows her a higher benefit at all ages than if she were to retire sooner. Scenario three shows her continuing to work until 67 but also shows that if she starts Social Security at 62 that she would have to pay it all back.

In the video below, we go into more detail regarding these scenarios and also detail what happens if she were to wait to get remarried until after age 60. There are many more options for widows and widowers than couples or singles who do not have spousal benefits. If you have lost a loved one, it makes even more sense to look at all the options available and plan ahead of time so that you do not lose benefits.

Articles and videos will help you make sense of much of this for yourselves, but none of us know where our blind spots are. If you would like someone to help you uncover some of these blind spots and consider more than just one or two variables, it may be best to go over your unique situation.

Please feel free to reach out, and someone from our office can help make sure you do not miss out on many of these benefits.

Joe Franklin has been named by Forbes as one of Tennessee’s Top Advisors!

Franklin Wealth Management

4700 Hixson PikeHixson, TN 37343423-870-2140