This year has been a tempestuous one to date with early concerns about tariffs, foreign relations, budget cuts, and government layoffs. This is all a part of the Golden Playbook the Trump Administration seems to be following zealously.

When we know our playbook well, we can play the game more effectively. When we know all the team’s playbooks better than anyone else, we can have greater assurance of victory. The U.S. playbook is not hidden. Those who are aware can follow the designs and seek to profit until the Administration shows they have changed the game plan. Year to date, Trump has been seeking to fulfill his promises and follow through on this plan, and this plan has its effects on the market that can be predicted based upon the actions taken.

Trump’s Golden Playbook – “The Mar-a-Lago Accord”

Last November, Hudson Bay Capital released a 41-page document that outlined a plan to restructure the global trading system. “A User’s Guide to Restructuring the Global Trading System” touches on everything from US debt to interest rates to re-shoring of US manufacturing, but with a central idea of a “Mar-a-Lago accord” built around tackling dollar “overvaluation” and what the author Stephen Miran wrote could be “a 21st Century version of a multilateral currency agreement.”

The Trump Administration has been following this playbook consistently ever since the inauguration. Mr. Miran was named as chairman of the Council of Economic Affairs in January and has more recently been installed as a member of the Federal Reserve Board of Governors in September.

In Miran’s paper, he argued that tackling the currency question could rebound in America’s favor on a variety of fronts, from the national debt to national security arrangements to providing a boost to US businesses.

The goal is to ensure the dollar remains supreme as the global reserve currency while at the same time correcting what is viewed as an “overvalued dollar” that makes US manufacturing less competitive.

The late 2024 article explained that the US could convince other countries to help with this devaluation in exchange for security guarantees or a pledge to drop punitive tariffs. Some speculate the US may want to provide protection guarantees for countries like Taiwan, South Korea and much of Europe in exchange for them agreeing to purchase century bonds when interest rates come back down.

Miran called this a “multilateral” approach to a new trading landscape.

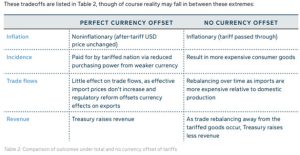

He outlined the tradeoffs of a weak dollar combined with tariffs to accomplish the goals of paying back U.S. debt with a devalued dollar, increasing exports of lower-priced goods, allowing for the re-shoring of jobs with a renewed focus on productivity over consumption, and a reduction of inflationary pressures with optimal currency offsets.

A perfect currency offset would be designed to allow higher treasury revenues for the United States, greater trade exports, and muted impact on the cost of goods and services.

In recent months, Trump has talked about using a U.S. sovereign wealth fund to force the dollar lower by purchasing massive amounts of foreign assets. The U.S. has had many concerns about the Chinese imposing a weaker Yuan on the rest of the world over the last decade, but it seems we will be taking a page from their playbook. In a recent speech Trump said, “It doesn’t sound good, but you make a hell of a lot more money with a weaker dollar. Not a weak dollar, but a weaker dollar than you do with a strong dollar.”

Making More Money with a Weak Dollar

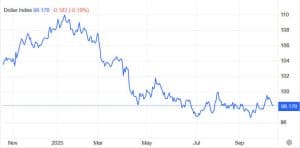

Trump’s Devaluation of the Dollar has been going to plan so far. During the first half of 2025, the US dollar had fallen at the fastest rate of the last fifty years. We have to go all the way back to 1973 to find a time when the dollar fell faster. When the dollar falls by 10% versus all the other currencies around the world, as it did earlier in the year, the effects can be seen easily in the markets and eventually in trade and inflation effects.

You can learn more about Trump’s plan to devalue the dollar by watching the video above.

The Tariff agreement that the U.S. made with Europe looked to be a big win for America, but there are ways that Europe may come out ahead because of the weaker dollar. A weak dollar allows for more jobs flowing into the U.S. and allows our exports to be cheaper versus the rest of the world, providing a boost to U.S. trade. A weak dollar, especially combined with tariffs, makes foreign goods and travel abroad more expensive. But how does this affect investments?

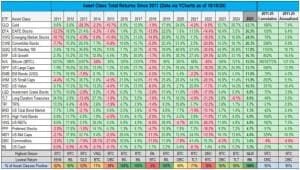

Because other currencies are getting stronger versus the dollar, investors seek investments in those assets that will increase in value the most. Funds will flow out of the weaker currencies into the stronger currencies. Europe and parts of Asia have been the biggest winners in the flight of capital year to date with Poland, South Korea, Vietnam and Greece standing out the most.

Non-US stocks have outperformed US stocks by over 13% so far this year. Not much outperformed Europe during the first part of the year and Emerging Markets have been playing catch up in more recent months.

Gold is in. Bonds & Bitcoin are Out?

Foreign markets cannot hold a candle to gold in 2025, however. A fixation with gold is common when the dollar starts losing value. However, over the last decade, most have chosen to focus on Bitcoin and other digital currencies as what many see as an improved store of value.

Yet, investors do not buy digital currencies for protection during weak economies or weak markets. Digital currencies do well during “Risk On” environments. This is the first time bitcoin has not outperformed all else during the third year of the four-year “halving cycle”. This could be a sign that the upside for Bitcoin going forward is not as great as it has been during past cycles. It could also be a sign that the “smart” investors are more concerned about protection and feel that gold provides more stability going forward.

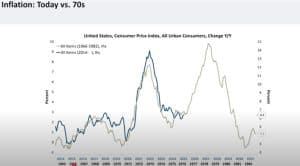

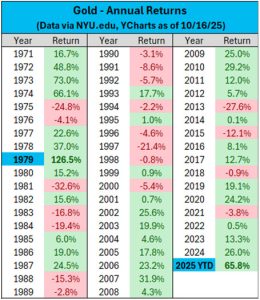

Gold was the best-performing asset class for investors in the 1970s and the second best performer during the 2000s. Gold has already grown more in value in 2025 than any year since 2000. We have to go back to 1979 to find a better year for gold.

2025 seems more like 1974 than any other year with respect to gold. In the early 1970s through 1973 inflation grew out of control. Inflation tempered in 1974, much like it has recently, but gold continued to march higher than it has now.

Yet gold tends to peak when markets bottom. Many feel that markets may bottom in 2026 as unemployment continues to rise and give way to fears of recession. Gold may not peak until we see a significant drop in the markets as we did in 1974. The following years (1975 and 1976) provided a period of gold selling prior to the biggest gold rush seen this half century.

When Bonds Outperform Gold

Historically, gold and treasury bonds do well during “Risk Off” environments. We expect bonds to potentially perform even better than gold over the next year. Gold does well when investors grow concerned about dollar devaluation, but also when investors grow wary of recession. Bonds do well when the Federal Reserve starts lowering rates, and this tends to happen only when they become more concerned about recession and unemployment than they are about inflationary forces.

Unemployment bottomed in 2023 and has been rising since then. In 2024, we witnessed government jobs reach close to 25% of all new hires in the economy. That changed in 2025, but severance checks have kept these former government employees off the unemployment rolls. This is likely to change soon, and the Fed is set to lower rates as they do.

Most bond managers are expecting rates to come down another 0.75% between now and the end of the first quarter of 2026 and 1.5% by the end of 2026. When this has happened in the past, bonds do well, and long-term treasury bonds do exceptionally well.

When we see a one percent drop in interest rates, long-term treasury bonds have historically risen by over 20%. But what happens if the economy falters? During the last two recessions, the Fed effectively lowered rates to zero.

We do not expect interest rates to be at zero again anytime soon, but a 3% drop will likely give us a return of greater than 60% in long-term treasury bonds. Trump is calling for this 3% drop to provide lower borrowing costs for the U.S., more affordable cost of capital for businesses, and more affordable mortgages. No one knows exactly what will happen, but we know what the Trump Administration wants to happen and its best to position ourselves to profit from what the government is working to accomplish.

To learn more about Gold and Bonds in 2026 and the Trump Era vs. the 1970s, watch the video below.

Joe Franklin has been named by Forbes as one of Tennessee’s Top Advisors!

Franklin Wealth Management

4700 Hixson PikeHixson, TN 37343423-870-2140