When it comes to retirement planning, most people focus on how much they’ve saved.

But in reality, one of the biggest financial differences in retirement comes down to something far more strategic:

The order in which you withdraw your income.

Get this wrong, and you could unintentionally increase your tax bill, reduce your lifetime income, and leave less behind for your family.

Get it right, and you can create a more tax-efficient, predictable, and even generous retirement.

Let’s walk through how this works.

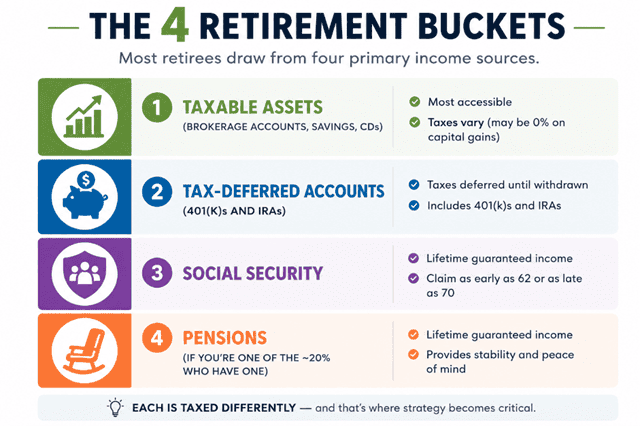

The 4 Sources of Retirement Income

Most retirees draw from four primary income buckets:

- Taxable assets (brokerage accounts, savings, CDs)

- Tax-deferred accounts (401(k)s and IRAs)

- Social Security

- Pensions (if you’re one of the ~20% who have one)

Each of these is taxed differently—and that’s where strategy becomes critical.

Why Withdrawal Order Matters More Than You Think

A common mistake I see is people turning on Social Security and pulling from their 401(k) at the same time.

On the surface, that feels safe. You’re getting income from multiple sources.

But here’s the problem:

👉 That combination can dramatically increase your tax burden.

In some cases, a $20,000 withdrawal can effectively be taxed like $37,000 due to how Social Security taxation works.

That’s not intuitive—but it’s very real.

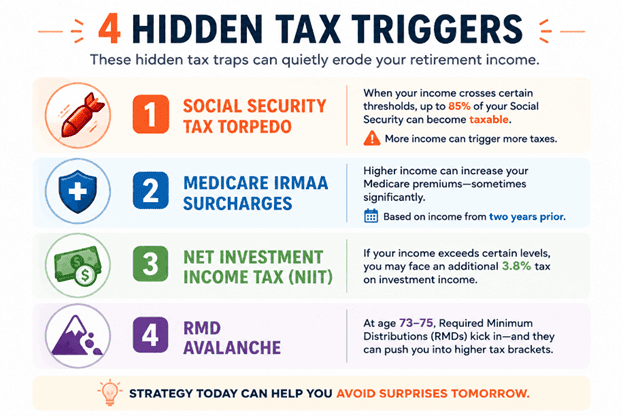

The 4 Hidden Tax Traps in Retirement

If you want to optimize your retirement income, you need to understand these four key tax triggers:

1. The Social Security Tax “Torpedo”

When your income crosses certain thresholds, up to 85% of your Social Security becomes taxable.

This can create a ripple effect where additional withdrawals trigger even more taxes.

2. IRMAA (Medicare Surcharges)

Higher income can increase your Medicare premiums—sometimes significantly.

And here’s the catch:

👉 These are based on income from two years prior.

3. Net Investment Income Tax (NIIT)

If your income exceeds certain levels, you may face an additional 3.8% tax on investment income.

4. The RMD Avalanche

At age 73–75, required minimum distributions (RMDs) kick in—and they can push you into higher tax brackets if not planned for early.

The “Golden Window” Most People Miss

One of the most powerful planning opportunities happens in what I call the:

Golden Window

This is typically the period:

- After you retire

- Before you turn on Social Security

- Before RMDs begin

During this time, your income is often lower—creating a unique opportunity to:

✔ Withdraw strategically

✔ Convert assets to Roth

✔ Stay in lower tax brackets

This window can start as early as age 55 and extend into your late 60s.

And it’s one of the most underutilized strategies in retirement planning today.

A Smarter Withdrawal Strategy

While every situation is unique, a tax-efficient framework often looks like this:

Step 1: Use Taxable Accounts First

Draw from:

- Brokerage accounts

- CDs

- Savings

Why?

Because:

- You may pay lower or even 0% capital gains taxes

- You avoid triggering Social Security taxes (if not yet claimed)

Step 2: Tap 401(k)s and IRAs (Strategically)

Before Social Security begins, withdrawals from these accounts:

- Don’t trigger Social Security taxation

- Can be managed within lower tax brackets

This is also the ideal time to consider Roth conversions.

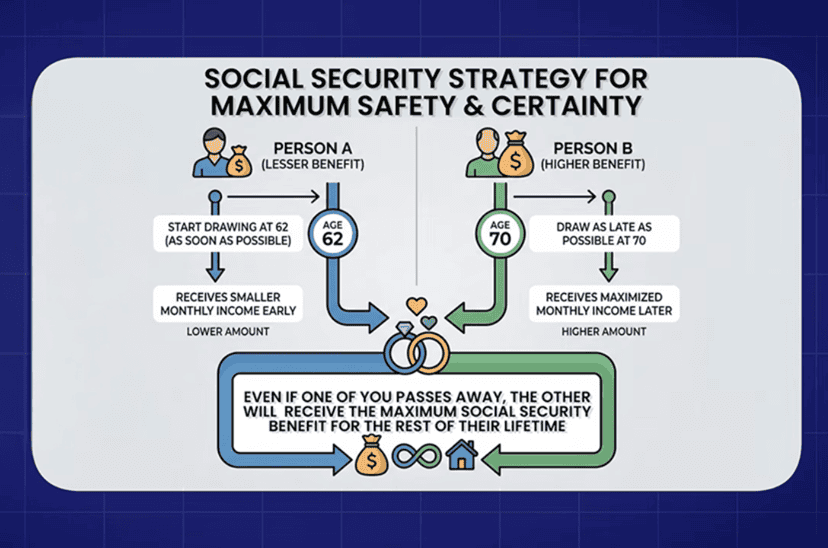

Step 3: Delay Social Security (When Appropriate)

Waiting can significantly increase your benefit.

In fact:

👉 Waiting until age 70 can increase your benefit by up to 77% compared to age 62.

For married couples, a common strategy:

- Lower earner claims earlier

- Higher earner delays

This can maximize lifetime and survivor benefits.

Step 4: Coordinate Pension Timing

If you have a pension:

- Evaluate whether waiting increases the payout

- If not, it may make sense to start earlier

Pensions can also provide stability, allowing more flexibility with other assets.

The Bottom Line

Retirement isn’t just about building wealth.

It’s about keeping it—and using it wisely.

The order you withdraw your income can impact:

- Your taxes

- Your lifestyle

- Your healthcare costs

- Your legacy

And most people don’t realize they’ve made a mistake until it’s too late to fix it.

Final Thought

If you’re within 5–10 years of retirement—or already there—this is one of the most important conversations you can have.

Because the goal isn’t just to retire.

It’s to retire with confidence, clarity, and control.

Call to Action (Website / LinkedIn)

If you’d like help building a tax-efficient retirement income strategy, we’d be glad to help.

Give us a call: (423) 870-2140