This past years stock market surge and resurgence of IPO activity takes me back a few years to when we were all still working for a parent company that was significantly involved in underwriting and pushing out IPOs as well as secondary offerings to its financial advisors and customers. Making a public market for companies to be able to create capital to expand and improve is a very worthwhile and necessary function. However, common practices and the inherent conflicts of interest between issuing companies, underwriting brokerage firms and the retail customer can be quite staggering.

Usually this is seen when “Wall Street” research is unashameably positive prior to companies placing offerings with the underwriting firms. Customers are not always on the lookout for research that may be biased by brokerage firm’s investment banking desires. This does not come to a head until the market suffers a dramatic fallback. We saw this during the technology bust where “rock star” analysts who helped generate millions of dollars in investment banking revenue fell from grace. Likewise in 2008 we may remember some firms who offered GM bonds as well as Freddie Mac and Fannie Mae bonds to the public mere weeks before these firms actions as well as the governments actions made these securities largely worthless. Josh Brown of the “Reformed Broker” and others have blogged about this consistently over the last few years.

The impetus for this post was a policy alert that came across my desk last week which stated that many firms would start clawing back compensation from certain IPOs if clients sold the shares within 90 days of the offering, particularly closed end funds. With most IPOs there is a “penalty bid” period where if the IPO is sold back into the market, the financial advisor will either not be able to get as many IPO shares in the future or the advisor will lose previous compensation from the original IPO sale. In some cases, if the shares are up over a certain amount, this penalty bid period will be waived.

The other side of the coin relates to allocations provided by the syndicate IPO department to financial advisors and thier clients. At one firm we are very familiar with, the syndicate department allocated future IPOs based upon how many shares a financial advisor’s clients have bought in the past and how long they held onto them. Typically the more attractive the company IPO is, the harder it is to get many shares on the allocation. So the game becomes increasing the score by allowing clients to buy lesser IPOs so that they can get the better IPOs in the future.

Closed End funds are one type of IPO that is more available than any other type of IPO in that they issue as many shares as the financial advisors can place with clients. What tends to happen is that these funds come out at a price which is higher than what it is worth and within 60 days trades to less than what it is worth. This is typically after the penalty bid period is over. So advisors are encouraged to promote these closed end funds so that they can get a higher allocation of good IPOs for clients and are trying to find the best ones that hopefully will not stop dropping after 60 days or get their clients out of these funds before they drop too much.

We eliminated our need to play this game where the inherent conflicts of interest are so great by re-affiliating with an independent broker dealer that does not underwrite any of these types of securities. We don’t eat too many sweets or unhealthy foods if we do not keep them in the house. Likewise, we made a conscious decision to get rid of these types of conflicts of interest in our practice by affiliating with a firm that does not provide these “junk food” products for our consumption.

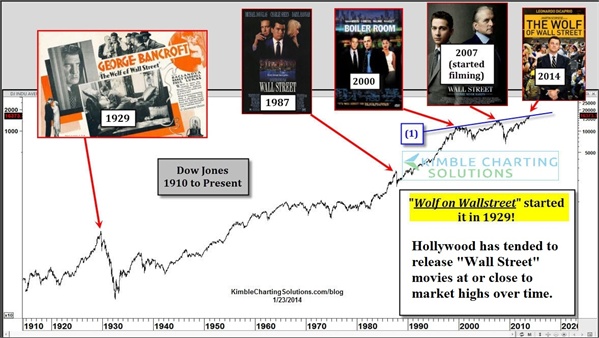

Since then, Hollywood has created several movies about Wall Street, and many could say that they have been released at or close to respective market highs. Eighty four years after the original “Wolf on Wall Street” movie is released, we have another more flamboyant version. What does this mean for the markets in the near future?

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are un-managed and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.