“Forecasting is difficult because we don’t know what is going to happen in the future” – Yogi Berra

It’s interesting how people tend to extrapolate into the future. They erroneously assume that what has happened recently will continue at the same pace for the foresee-able future. It is a behavioral trait that many exhibit that can be hard to temper. When working with clients, we work to help them keep a long term perspective rather than looking just at the last 2 months or 2 years.

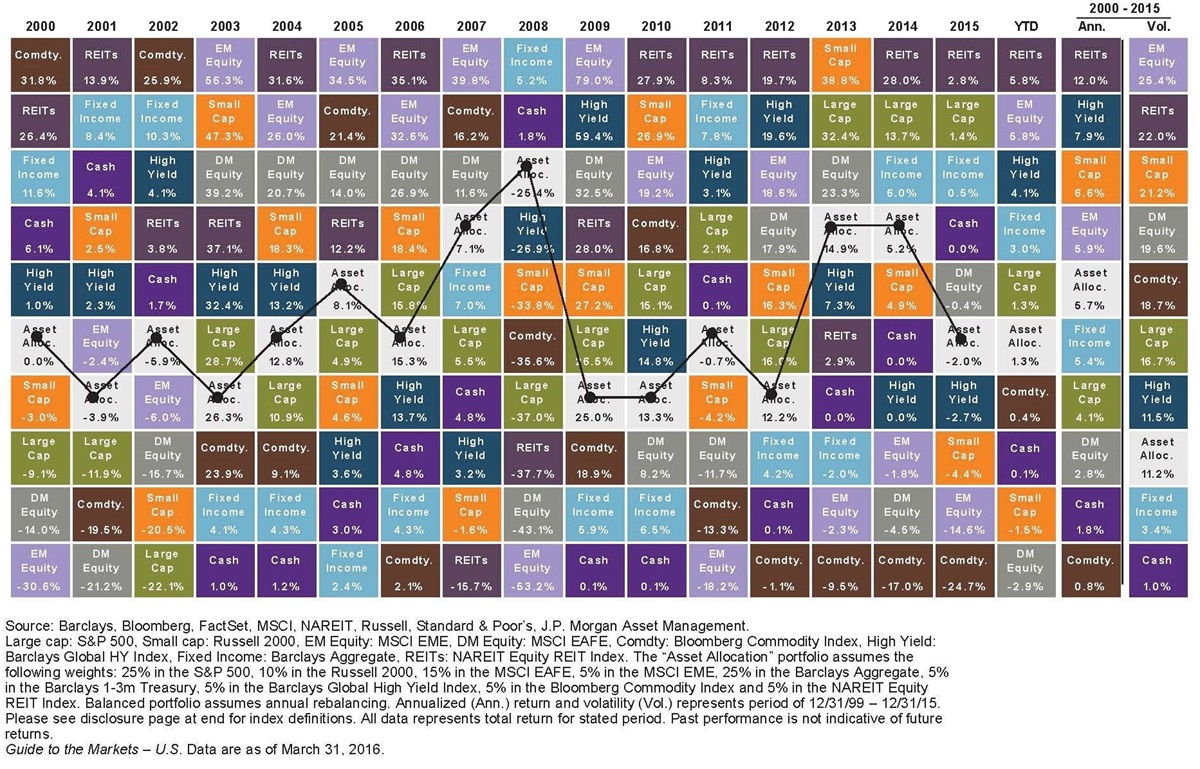

A client we recently brought on board was reflecting on the experience of his first couple of months with us. His experience so far has been to see his portfolio gain over 12% in these months. Although we cannot take credit for his becoming a client at such a fortunate time, nevertheless his thoughts on the subject were “Wow, if we continue at this pace, I’ll double my portfolio in two years!” We were quick to bring his expectations down and let him know that his timing couldn’t have been much better. For diversified investors, (as noted in the chart provided by J.P Morgan below) a diversified portfolio (55% equities, 35% bonds, 10% inflation hedges) would have averaged less than 6% over 15 years starting at the beginning of 2000.

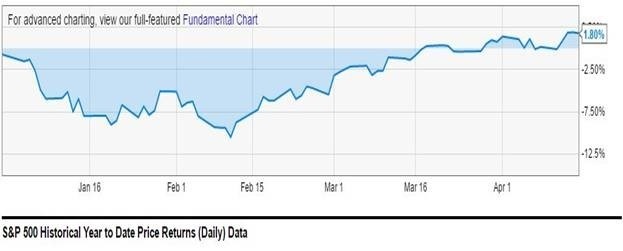

Of course, prior to mid February, many investors suffered through the worst start to the year that we have ever seen for the markets. Many were thinking that they cannot handle staying invested if the fallout continued. We were quick to point out that these pullbacks happen almost every year and most years investors who don’t abandon ship are rewarded with positive returns.

No one predicted what we experienced in the first two months of 2016. By February 11th, 2016 (basically the middle of the first quarter) the S&P 500 was down over 10% for the year, logging the worst start to a calendar year in history.

By the end of the quarter, the S&P 500 had not only recovered, it was positive and declared one of the biggest quarterly reversals since 1933.

FOLLOW THE EARNINGS

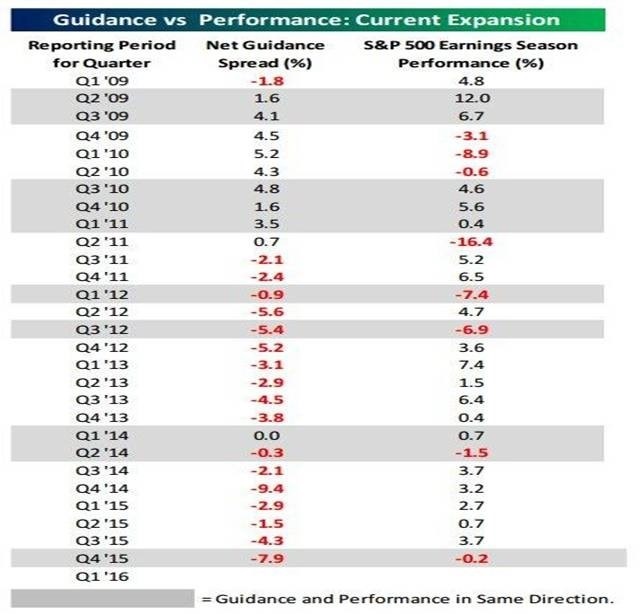

Last week was the start of the first quarter earnings report season, with average analyst expectations for earnings showing declines anywhere from off 7% to off 9% compared to last year. Those negative estimates have been rising over the past number of weeks. Many pundits suggest that unless earnings, and forward guidance, are better than expectations, the equity markets will travel back down again. But we feel it is more profitable to be somewhat contrarian and become slightly more bullish as others get more negative. Low expectations tend to set us up for better times ahead. As the good folks at Bespoke Investment Group note (as paraphrased):

Given that we track this kind of information on a regular basis, we looked to see how the S&P 500 performed during earnings seasons (six-week period beginning the Friday before Alcoa report) since the start of 2009. . . . Of the 28 reporting periods, the direction of the market during earnings season was the same as the net guidance spread only ten times (36%). Furthermore, in the last twelve quarters (three years) the guidance spread has been negative eleven times, and the S&P 500 has been down during the corresponding reporting period just once. As we have discussed in prior reports on the subject, when it comes to earnings season, what really matters is expectations heading in. When expectations in the form of analyst revisions are negative leading up to the start of earnings season, equities typically rally during earnings season, while positive sentiment leading up to earnings season sets a high bar to surpass.

If we look at these numbers going back a little further and include most recent data as well, we can see that out of 18 periods when the guidance spread has been negative, the market has been positive 14 times. It is interesting to note that since the beginning of 2009 that when the guidance spread has been positive, the markets are up 56% of the time but when guidance spreads are negative (lowered expectations) the markets are up 78% of the time. This suggests the current negative guidance may be more beneficial than many believe.

THE SONG REMAINS THE SAME?

Markets tend to move in cycles. Over the last few years, U.S. large companies and REITs have outperformed most other investment classes. Outside research and our internal research leads us to the conclusion that the next 10 years will look similar to the period from 1998 to 2007. There will be differences this time around and we doubt we will see another bubble quite as overblown as what we saw in late 1999. The music of the markets rhymes but does not repeat itself.

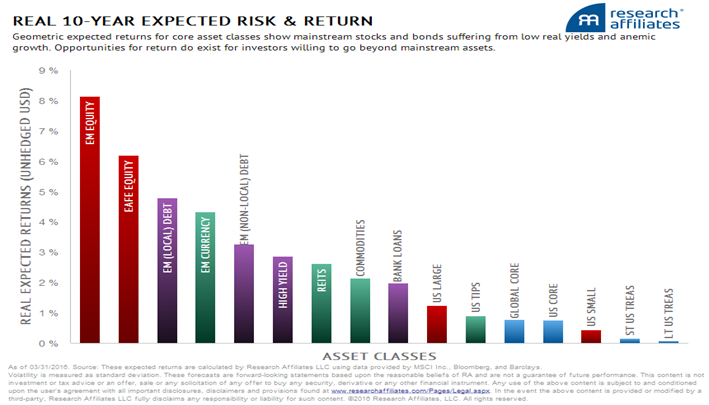

We believe that gains from investing in U.S. stocks and REITs will be less inspiring than they have been recently and that it may be time to look for emerging markets, energy and selected developed foreign markets to take leadership. Those who fail to diversify outside the U.S. may find themselves wishing they had after a few years. The following chart shows the expected return from Research Affiliates for multiple asset classes based upon current valuations.

We continue to see resemblances between our current market environment and what we experienced in 1998. We wrote about this extensively in January (see Did you Lose Your Head this January). One does not need to look very far to see how oil prices, the energy sector and emerging markets fared over the next 10 years starting at the end of 1998.

REPLACING LOW TURNOVER WITH “NO TURNOVER” IN TAXABLE ACCOUNTS

At the end of last year we noticed that many mutual funds were going to be paying relatively large capital gains even though they were under water in 2015. We shifted out of these funds just before they were to pay into other similar funds and then shifted back after the pay date passed. We owned many low turnover funds that were historically tax efficient but they were paying large taxable distributions nonetheless. For this reason, we are embracing index ETFs to a greater degree for clients with taxable, non-retirement accounts. We feel we can offer more diversification utilizing both passive and active strategies.

For more on this strategy – please follow this link.

LADDERING STILL WORKS

Investors seeking more certainty can typically find it by laddering a portfolio of bonds and other fixed income vehicles. In a stable or rising interest rate environment this works to provide more income over time as the lower yielding bonds mature and are replaced with new bonds at the end of the ladder that pay a higher interest rate.

For more on this strategy – please follow this link

PERSONAL PENSIONS PROVIDE MORE CERTAINTY

Fixed income from treasuries is approaching a seventy year low. We also saw an uptick in defaults from high yield bonds in 2015, primarily as a result of the fallout in the energy sector. In order to get the income needed for their golden years, many retirees are forced to take more risk and deal with the increased volatility.

With U.S. Markets expected to return less than three percent (based upon the chart above), a four to seven percent lifetime income stream starts to look more appealing for those living off their accumulated assets.

For more on this strategy – please follow this link.

FOR THOSE OF YOU WHO ARE STILL WONDERING ABOUT NUMBER 2

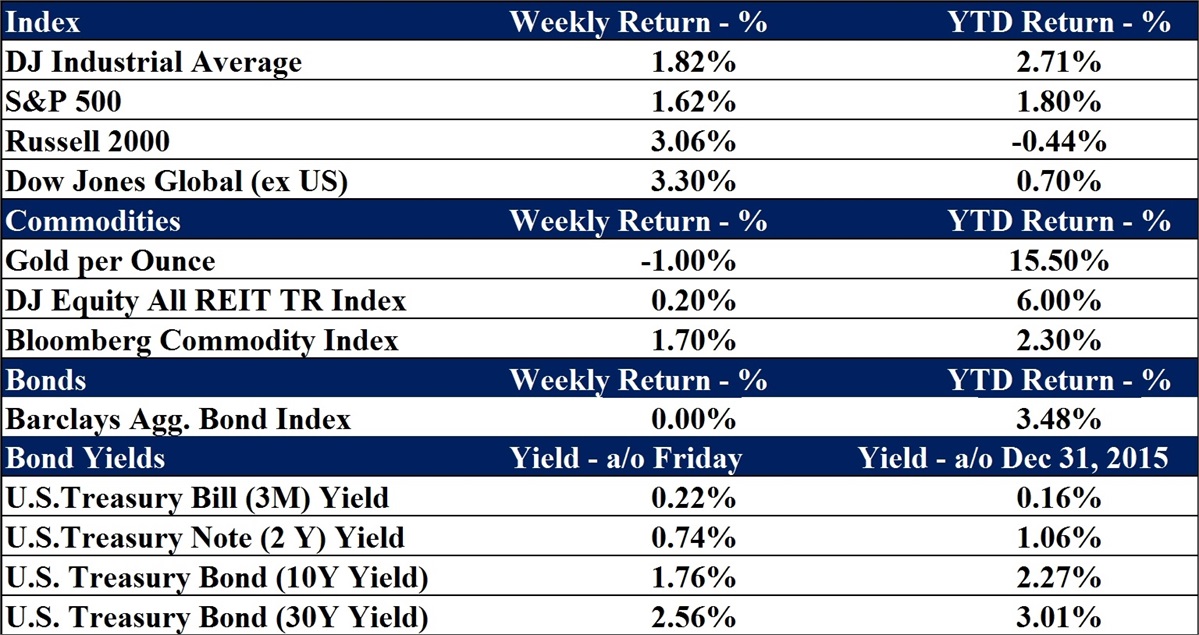

Data as of 4/15/2016

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, a registered investment advisory firm in Hixson, Tennessee. A 20-year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request