A few weeks back, Jennifer and I took our kids to Boca Raton for spring break. This break just happened to coincide with an LPL Financial trip rewarding its top ten percent of financial advisors and it was the kids first trip of this kind since Sydney and Jack were little. I enjoyed getting to explain to them a little more about my work and what the conferences and trips are all about when we get to learn and enjoy a little time away from the office.

While in Florida, I had the chance to hear Jack Nicklaus speak on what he felt was most important during his golf career and now that he is trying to mentor his children and younger golfers. Below are just a few of the nuggets that were impressed upon me.

“There is no excuse for not being properly prepared” – Jack Nicklaus

Nicklaus was well known for spending more time before a big event at the course than any of his competitors. He had a habit of arriving a week ahead of time to make sure he understood the course and took time off just before to relax and prepare mentally. He related how he brought Gary Player along to help him prepare for the Masters a week early and how Player ended up winning that year. Nicklaus took home the trophy more often than most others, but when he impressed upon his friends and competitors how important the preparation was to him, they were able to improve their game as well.

Lately in our classes at Cleveland State, we have been stressing with several case studies how we have been able to provide much more certainty for our clients through proper planning. We stress how proper planning is often more important that earning an extra percentage point on investments and can add more certainty to their financial future. Maximizing Social Security income, restructuring plans to minimize taxes over time, utilizing correct liquidation strategies and tax efficient savings as well as making sure that clients know their family index number are all vitally important. These planning strategies enable clients to live out their retirement years with peace of mind and are just a few things we utilize to enable clients to have more in retirement than earning a little extra on their investments. Creating a plan and sticking to the plan are the most important aspects of our clients being successful over the long run.

The Power of “Focus”

Nicklaus also talked about how he always made sure to maintain his focus. He felt that “playing golf” was always the most important thing, above endorsements or any other business ventures he might find himself involved in. He told us that he made the most money per hour “signing my name”, but that only came about because of the focus on playing golf.

My personal focus is to inspire and empower everyone to be all they can be whether they be clients, team members or friends. Since my father’s passing one aspect of this has been to rescue as many people as possible from the troubles my brother and I experienced with the probate process and inadequate implementation of good planning. We want to ensure that assets pass to the next generation with as much ease as possible and that children and grandchildren are set up for success rather than hobbled by the sense of entitlement that sometimes comes with inherited wealth.

Be Patient

When it comes to investing, we also believe that investors should stick to the plan for their future. We like to stress that “one bad year does not derail a good investment plan nearly as much as switching tracks on route to our destination”. Any good strategy or portfolio manager is going to go through exceptionally good periods and bad periods as well. Often the best periods come immediately following the rough patches, as anyone in our Global Income portfolio can attest from the difference in 2015 and 2016 results. As long as we stay diversified and remember to maintain an even temperament, we can pull ahead in the long run. It’s our behavior during the difficult times as well as the “can’t lose” periods that determines our success more than any other factor we can point to. Nicklaus related his advice to Rory McElroy recently when Rory was going through a slump. He told him to, “Be patient and stick to your strengths. Patience is a great virtue. Your game will come along if you are patient.” It seems he didn’t need to be too patient because he won the next week, but he also did not hurt himself by forcing things.

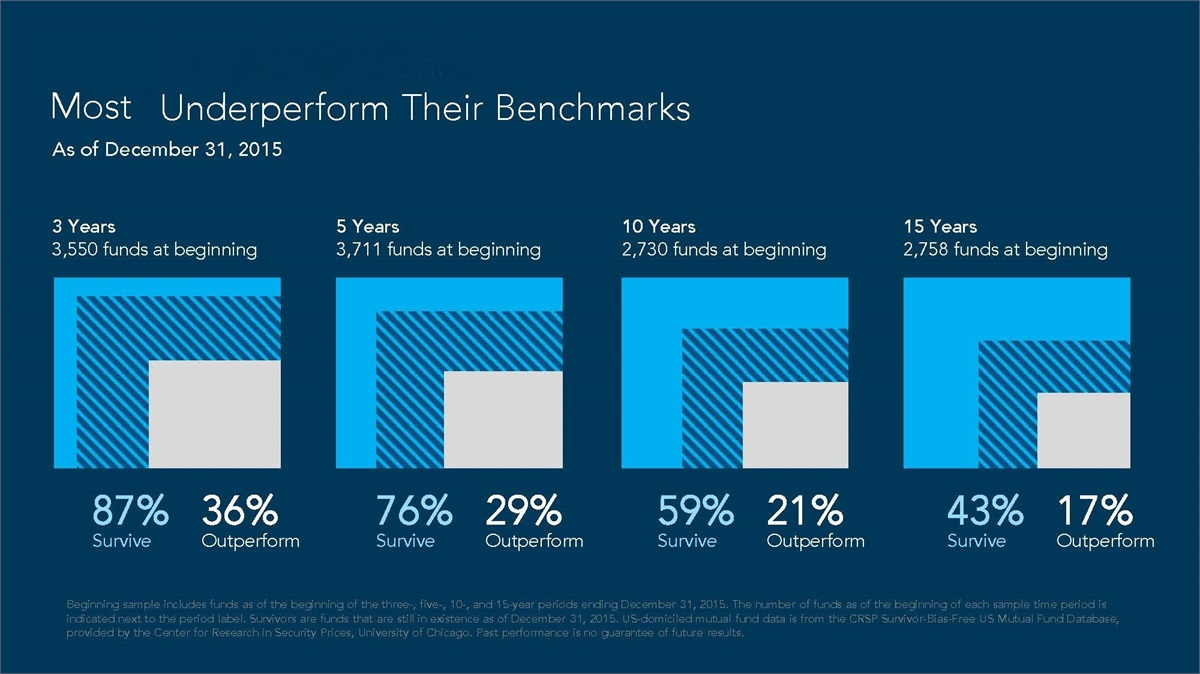

The chart below showcases how most portfolio managers fail to beat the indices or even stay in business over a fifteen year period. One study shows that over the fifteen year period ended in December, 2015 that of all funds in existence in 2000, only 43% survived the next fifteen years and only 17% managed to outperform their benchmark. Some would think that based upon this evidence that it is fruitless to look to find managers who can outperform. But as we noted in our ”Are You a Believer?” article last month, those who seek the answers that elude many are more apt to find them than those who strive only to be average.

“I did not have a fear of winning. It takes courage to win!” – Jack Nicklaus

We find that asking the right questions often leads to better answers. The questions to ask in this case are “What are the commonalities found in those portfolio managers who consistently outperform their benchmarks?” and “What should we be looking for in portfolio managers today to make a determination that they can outperform in the future?”

We have found five primary characteristics, backed by extensive research over time showcasing which managers can and do outperform over time. They can be found below.

How Low are the fees and expenses?

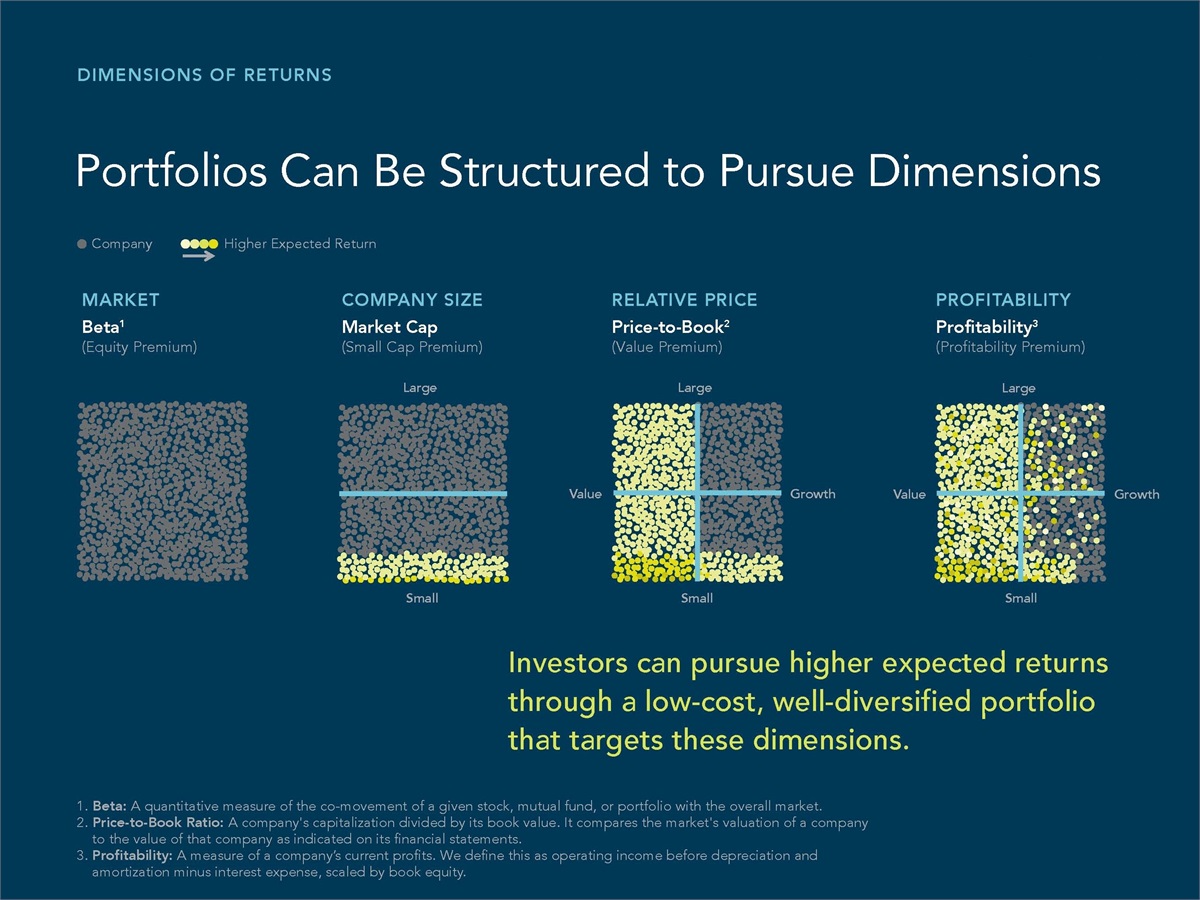

All other things being equal, lower expenses provide better performance. A recent Morningstar study from December of 2015 showed that the difference in returns between the U.S. stock portfolios with the highest expenses and those with the lowest expenses was over 2 percent. In taxable accounts, low costs and low turnover also tends to be more advantageous when accounting for investment time frames and capital gains exposure. For this reason we utilize these low turnover, low expense portfolios extensively in taxable accounts. These strategies that utilize enhanced indices are designed to minimize the drag of expenses and turnover while at the same time benefiting from lower volatility and strategic shifts to take advantage of market inefficiencies.

For more on pursuing these dimensions of low cost out-performance please click on the picture below.

While this low cost factor is often the easiest to measure, and has garnered much attention over recent years, we feel that investors should not limit their selection criteria to this one variable.

Does the portfolio manager own a significant stake in what they are buying?

Managers who own significant amounts in their own portfolios tend to be more focused on long term growth of investor’s capital than the career risk associated with not “hugging the index” or growth of assets and profits at the expense of the investor’s future returns. One study conducted in 2005 over a relatively short period of time showed that managers who are personally invested outperform their peers by an average of 1.44% per year. Another study identifies that those portfolio managers with the highest manager ownership and the lowest expenses have outperformed over time. This study shows the portfolio managers that are in the top 25% for ownership and the bottom 25% for fees and expenses have outperformed their indices 86% of the time over rolling 10 year periods and 72% of the time over rolling 5 year periods during the 20 year study ending in December 2016. After expenses this out-performance equates to well over 1% on average after all expenses.

We adhere to this philosophy also and intentionally constructed our models to be able to buy and sell securities for our clients at the same time these trades are conducted in our own portfolios. We are invested alongside clients in this respect, eating our own cooking.

For more on how manager ownership affects results, please click on the picture below.

How often does the portfolio change? What is the average turnover?

How often does the portfolio change? What is the average turnover?

The turnover ratio is the percentage of the portfolio’s assets that are bought and sold in any given year. The best portfolio managers tend to trade less often and hold for the long term. Waiting for the fat pitch has proven to be more important than continually being active. Lower turnover also means lower trading costs. Trading costs include not only the out-of-pocket fees and commissions paid to market intermediaries but also market impact because a large transaction can significantly affect the price of the stock being bought or sold. During the twelve year period ending in 2006 a recent study showed the 20% lowest turnover portfolios showed performance 1.78% higher on average than the 20% highest turnover portfolios.

We wrote about this extensively in our article “Waiting for the Fat Pitch” a couple of years ago.

How much does the portfolio differ from the index?

An active manager can only add value relative to the index by deviating from it. Managers can be found at various ranges across the spectrum ranging from indexes to enhanced index and smart beta strategies on the passive side. There are active managers who are “closet indexers”, choosing to invest in the index but only make a few minimal changes hoping this will help them slightly outperform. Those who truly add value are the ones who differ the most from the index with original ideas and strategies leading them to investments where they have strong convictions. As of 2016 roughly 30% of U.S. Large company active equity managers (and roughly 20% of assets under management) show overlap of the index of 20% or less. One study concluded in 2013 titled Active Share and Mutual Fund Performance showed that those funds with less than 20% overlap outperformed their benchmark by an average of 1.26% per year after fees and expenses for the 20 year period ending December 31st, 2009. We find that these types of managers have outperformed over a long period of time, but many have under-performed over shorter periods such as in 2014 and 2015.

Funds that display these characteristics typically have low correlations to their respective benchmarks and a high percentage of the portfolio concentrated in its top ten holdings. We obviously prefer these types of portfolio managers in our MF models and anyone can easily see that both our Global Income and Global Long Term Growth models fit the bill.

For further studies on this, feel free to click this link.

How well does the portfolio manager protect during downturns?

When considering which portfolio managers are best suited for the future it is best to consider how they perform over an entire market cycle. As we wrote last month, many of the high flying managers of the late 1990s fell from grace in the 2000s and many are no longer in business. Some managers that many felt had lost their edge at the time showcased their expertise coming out of the dot.com craze and rewarded investors during the “lost decade” when large company U.S. investors showed diminishing value in their portfolios. The best portfolio managers tend to minimize losses in bad periods. They may not reward investors quite as extensively on the upside but show their superiority over an entire market cycle. As we noted in our article last month, the ten “New Super-Investors” noted in Lowenstein’s article under-performed in one year out of three on average and four of them “had each under-performed for four consecutive years from 1996 to 1999. Successful investing thus requires not just patient managers but also patient investors, those with the temperament as well as intelligence to feel comfortable even when sorely out of step with the crowd.” As of late 2015, many of these managers may have also felt out of step. For most of them, this was a temporary phenomenon as the markets recovered in 2016. W.F. Sharpe found the persistence of risk adjusted performance calculated by the Treynor ratio showcased a greater than 70% chance of out-performance from one decade to the next. This is a relatively old study, but a good one nevertheless and is still referenced today.

W.F. Sharpe’s paper can be found by clicking on Warren Buffet’s two most important rules of investing below.

Being successful in our view involves not only creating a plan but sticking to that plan over the long run. Those who maintain a long term perspective and stay on track will come out ahead. When something else looks more enticing during euphoric times or the current track looks dangerous during pessimistic times, those with a long term perspective tend to come out well on the other side.

For more on all five factors, feel free to click on the picture above.

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, and CEO of Innovative Advisory Partners, a registered investment advisory firm in Hixson, Tennessee. A 20+year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.