In many ways, it seems like we have been rolling back the clock recently. Record government debt levels and unemployment rates for the U.S. bear a striking resemblance to the mid 40s. Current inflation rates are eerily similar to the mid- seventies. Technology valuations and the current unwinding of those valuations remind us of the early 2000 dotcom bust and Real Estate speculation and the impending slowdown reminds us of mid 2008. The bond market reminds us of little from years past, however.

In 2020, U.S. Treasury yields reached lows never seen before in history, and rates have risen at a rate never seen before as well. This has given rise to the worst bond market we have experienced in our lifetimes. Many have noted the bond market for 2022 is the worst in over two centuries.

Coming Attractions: The Best Bond Market in Two Decades?

The Federal Reserve Raised Rates Again this past week. We have not seen short term rates at over 4% since 2007. This brings bond opportunities and yields we have not experienced in close to 15 years. Because these yields are close to 15-year highs, we can look at laddering bond portfolios again. And strategies that were once very profitable and beneficial are back in favor.

Protection from Recessions and Weak Stock Markets

This year, bonds have not been a good hedge against weak equity returns. Why? Because the weak bond market has been the primary cause of weak equity returns. The most recent rally started when the bond yield peaked in June and ended not long after it bottomed at the end of August. We anticipate this correlation to continue until the economy slows more significantly. Inflation is likely to come down to the 4 to 5 percent range at the same time bond rates increase to slightly above this range. When this happens, the Federal Reserve will have less motivation to raise rates, especially if the unemployment rate starts looking worrisome. This will likely prove to be the peak in interest rates for this economic cycle. After bonds attain economic cycle peaks, it is a great time to look at moving capital to benefit from the imminent rate cuts and treasury bond panic buying that we typically experience toward the end of these cycles.

Past Bond Bonanzas

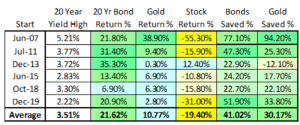

The best bond markets almost always follow the worst periods. These periods also tend to coincide with economic slowdowns. The chart above includes rallies for 20-year treasury bonds over the past 15 years from periods when the yields reached highs (bonds bottoming) to where these yields reached their subsequent lows (bond peaks). Two of these periods coincided with recessions and stock market panics where many would say the investing public was “panic buying” treasury bonds.

Buying treasury bonds after a period of sustained rate increases often proves to eventually provide profits much better than investing in equities as these interest rates come back down to earth. Many things can bring interest rates down to earth but deep recessions tend to do the most to cause interest rates to start dropping as the Federal Reserve starts pulling out the stops to lessen the pain.

It is clear the Fed is looking to kill economic growth in order to stave off inflation. Eventually they will go too far, and the pendulum will swing from inflation to possible deflation and deeper recession. This is exactly what happened in the mid-forties (the last time the U.S. debt to GDP was at these lofty levels). If interest rates drop back down to levels seen in 2020, coinciding with a deep recession, we are likely to see the best bond market in decades.

Absent this, a look at the bond market moves of the past 15 years may prove instructional. The 20-year bond rate is currently sitting at 3.87%. This is higher than any time since the beginning of the 2008 financial crisis. If we enter into a period that proves worse than the financial crisis or the pandemic, we will anticipate bond returns exceeding stock returns by over 50 percent. Other periods coming off a period of rate increases were also profitable.

Listen to the “Bond King”

“This is a very good time to buy bonds, and one of the ways I know that, is nobody wants to do it,” he said.

“The way it goes wrong is if the Fed collapses interest rates down to zero again, and then you’re going to have a lower income stream, but for the time being, it’s a very easy way of getting income,” said Gundlach.

For investors with low risk tolerance, he said a bank loan fund made sense. He said the spread to short-term interest rates is about 300 basis points. So if the Fed takes rates to 4%, the investor gets a yield of 7%, but can buy the bonds below 95, with a default rate of less than 1%.

I-Bonds are also making a lot of sense here considering they have been paying over 9% lately. The only problem is that the amount you can buy is limited.

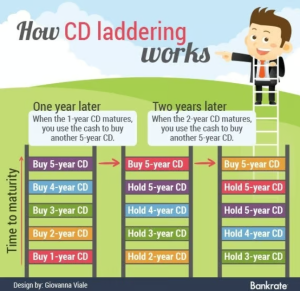

Laddering Bonds and CDs for Certainty

Lately we have been structuring portfolios with short term treasury bonds and CDs to lock in the income we may need for the next one, two, three or five years. With rates over 4% for CDs and government bonds in the 9 months to 2-year range, we can lock in gains and not have to worry about what may happen with the economy over the next few years. We have more arrows in our quiver now than we had a year ago. In 2020 and 2021, bonds looked very unattractive, and we actively looked at how we could lessen our exposure to interest rate risk at the same time we embraced investments that would benefit from inflation and raising interest rates.

This narrative may soon be changing. We want to still embrace investments that benefit from inflation and rising interest rates, but sometime soon, we may want to look at those investments that will benefit from a Federal Reserve that is actively trying to lessen the impact of a deep recession and shift to lowering interest rates and stimulative measures. We may not see bond lows with interest rates peaking until 2023, but we believe it is now time to think about buying bonds.

Carter Payne in our office has been sending out fixed income lists the last few weeks as bonds & CDs become more unattractive. Through this process, we are once again starting to see tax-free bonds paying over 5%. We recommend looking at short term CD and treasury bonds ladders and floating rate bonds for now, however.

For more on creating CD and treasury bond ladders, please feel free to give us a call. An article on this can also be found by following the link below:

Laddering vs. Chunking – How to maximize income utilizing this strategic process.

This chart shows how bonds fared vs. equities in during the Financial Crisis from mid 2007 to early 2009. It is interesting to note that gold fared even better than bonds during this period.

The stock market sold off significantly at the end of 2018 but investing in bonds or gold proved to protect portfolios.

Pandemic Panic: Stocks down over 30%, treasury bonds up over 20%.

Bonds outperformed stocks in 2014 but only after bonds significantly underperformed in 2013.

Toward the end of 2015 and in the first couple of months of 2016, energy prices declined significantly, China caused fits in the markets while bonds and gold outperformed equities by a wide margin.

In 2011, bonds and gold held up nicely while the stock market swooned.

Joe Franklin, CFP®President, Wealth AdvisorFranklin Wealth Management, LLC423-870-2140www.Franklin-Wealth.com