Better than the 4% Rule?

The 4% Rule has been ridiculed by Dave Ramsey multiple times over the years. Not long ago, Ramsey responded to a call in from a viewer who was asking about the 4% rule when taking withdrawals. He went ballistic. He called those who defend the 4% rule, “Stupid, Goobers and Morons.” He called the rule “Bogus” and told listener that everyone can withdraw 8% a year from their nest egg, claiming they will make 12% a year investing in stocks and that 12% – 4% inflation = 8%. While we definitely agree that 12% – 4% = 8%, we want to note that Dave Ramsey failed to recognize that there have been periods of time like the 2000s when the market (defined by the S&P 500) actually showed a negative return. Withdrawals from an all-stock portfolio when it is down can be detrimental to retiree’s financial health, especially when taking up to 8% and not seeing consistent positive returns.

Why Do Investors Choose to Lose Money After Inflation?

Inflation is a top item that affects someone’s ability to live comfortably in retirement. Inflation can prove to be much more damaging than rising interest rates. Talk to someone from Venezuela or Argentina, and they can tell you what it is like to see savings reduced to nothing while invested “safely” in banks earning a high interest rate. Rates in Argentina have recently been over 100% but with inflation exceeding 200%, you still lose. Negative “real” interest rates are common in most countries today. Commodities including energy, precious metals, agricultural products, and the like have been the only place to invest during these periods with the potential to overcome high inflation. Now that inflation has moderated and interest rates are now well over 5%, investors can win again in things other than commodities and other items that benefit from dollar devaluation.

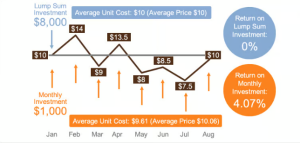

Reverse Dollar Cost Averaging – A Costly Strategy in a Volatile Market

Most are familiar with the benefits of Dollar cost averaging. Let’s say someone wants to buy Exxon Mobil stock at $90 a share starting in October 2012. $100,000 would have purchased approximately 1111 shares. The value of the shares at the end of September of 2022 at a price of $91.92 a share would equate to just over $102,000 (a gain of slightly over 2%). Investing $10,000 a year every October would buy more shares when Exxon is down and less when it moves higher. This alternate strategy would buy over 1452 shares which would be worth over $133,500 by September of 2022 (a gain of over 33.5%). This is a difference of over 3% a year in excess gains. This strategy works well in volatile markets and best in down markets when they recover.

Locking in Losses – Selling More Shares at the Low

Many retirees fail to realize they are falling victim to “Reverse Dollar Cost Averaging.” They sell more shares when the market is down, locking in their losses. A good fix for this fallacy is to only sell those holdings that are less volatile (rebalancing periodically to increase the allocation to more conservative holdings). In the past, the “safe” part of the portfolio has been bonds and other types of fixed income, but these “safe” investments have proven more volatile this past year as well.

Before the Fed started hiking, it made little sense to own cash equivalents when short term paper earned less than one percent and inflation was running hot. Until rates started to exceed the inflation rate, we felt commodities and other “inflation protection” options were the best options for portfolios. However, this has changed over the last couple of years. More options are available to us now that rates have increased. Interest rates for short term paper are 10 times higher than they were in early 2022 , opening our treasure chest of planning strategies. With higher rates, we can take advantage of strategies that did not make sense until more recently and may prove much more profitable for investors over the coming years.

An “Income Harvesting Strategy” Analysis (Our 2022 Analysis Updated)

Volatile markets encourage investors to shift to cash, bonds, and precious metals. Precious metals prove to be the most inflation resistant of these options. Cash, CDs and bonds made little sense until recently because “real” interest rates were still negative. But now that treasury bonds and CDs are paying over 5%, the rate of interest exceeds the stated inflation rate and we are rewarded for owning debt instruments again. The Federal Reserve vowed to beat down inflation by raising these rates and slowing the economy. If not for such high levels of fiscal spending, the economy would likely have already entered into recession. This spending has put the recession on hold but has rarely kept recessions away. Considering bonds tend to outperform during recessionary periods, keeping more funds “In the Barn” tends to be a winning strategy.

Today it makes much more sense to start looking at additional protection strategies for portfolios. “Income Harvesting” provides a “safe” storehouse of future withdrawals from cash equivalents during times of economic famine. When cash equivalents yield more than the inflation rate, we especially like the strategy. Locking in the income needed for one, two, three years or more provides income needed without having to sell off other portions of the portfolio at a loss, reducing the overall portfolio risk in the process. Those who are less familiar with the strategy may like to read more by following this link.

During market downturns, the overall portfolio loses less value than the other strategies (as shown in the chart below). During recoveries, it lags but not as much as a “Reverse Dollar Cost Averaging” strategy, which is also inherently more risky. Now that we can receive 5% or more from this storehouse of future funds, we can look at laddering a portfolio of CDs and treasuries to provide what may be needed if we encounter a longer downturn in markets and the economy similar to the early 1973-1974 period or the 2000-2003 period. Obviously, we like higher rates better than lower rates, but by laddering the portfolio we may also be able to realize higher rates over time as well. More on laddering bonds can be found by following this link.

Historical Performance of the “Income Harvesting Strategy”

versus “Reverse Dollar Cost Averaging”

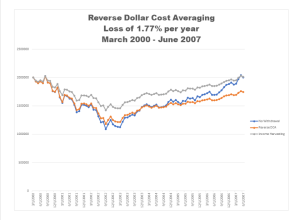

Our first two time periods show how the alternate strategies compare to buying and holding the S&P 500 Index. In these scenarios, we are assuming a family starts with a $2 million portfolio and draws 6% from the portfolio over a period of five to seven years. While we do not generally recommend a withdrawal strategy exceeding 4% of a portfolios value, this 6% rate is easier to model because it accounts for a withdrawal of $10,000 a month of retirement cashflow.

We compare the strategies by assuming the “safe” portion of the portfolio is invested in laddered CDs and treasury bonds earning an average of 4%. This is higher than we could earn from this type of portfolio until the last couple of years and is less than what was available during most of the 2000s but may have been harder to achieve from the 2010s until late 2022 prior to the Federal Reserve rate hikes. Withdrawals can be assumed to be spent, but for the purposes of this analysis we are showing them sitting in a separate account earning no interest.

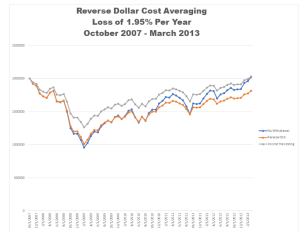

During the “dot.com” bust and the financial crisis, the “Income Harvesting Strategy” allowed investors to avoid selling stock investments at a loss with withdrawals coming from a laddered portfolio of CDs, treasury bonds, and higher interest money markets. Losses in the “no-withdrawal” example exceeded 40% in both periods but recovered more quickly as well. The “Reverse Dollar Cost Averaging” strategy shows a better return than “no-withdrawal” during the downturns and might be somewhat more appealing while the markets are weak, but it also fails miserably during the recovery phase. We can see by looking at the “Income Harvesting Strategy” that the overall portfolio suffers less in the downturn but also rallies less during the recovery phase. Returns are roughly similar to the “no-withdrawal” example but prove superior when adjusting for risk levels, considering much of the portfolio is “safely” stored away for future income needs.

If we encounter another period similar to the early 2000s or even the financial crisis and need to draw income from the portfolio, the “Income Harvesting Strategy” can be seen as superior. The strategy outperforms the “no-withdrawal” strategy until the markets have recovered and outperforms the “Reverse Dollar Cost Averaging Strategy” by a wide margin. Utilizing the “Reverse Dollar Cost Averaging Strategy” lost this family $200,000 or more in these two scenarios versus the other two strategies, equating to a slippage of over 1.75% per year.

When “Income Harvesting” Is Less Advantageous

From June 2013 through July of 2020, yields from CDs and treasuries with maturities less than 5 years started at one percent or less, and continued to decline. A 4% average yield could only be found if investors reached for yield by extending maturities or shifting to lower rated corporate bonds. The risk level in a portfolio increases when reaching for yield. Doing so during this period failed to reward investors as much as past periods as the increased risk levels made the bond portion of the portfolio take on volatility characteristics more similar to equities.

Moreover, because this period was mostly positive, the “Reverse Dollar Cost Averaging” strategy slightly outperformed the “Income Harvesting Strategy.” Some will argue that the “Income Harvesting Strategy” attained the same results with less risk, but the risk levels were continually increasing in order to attain the 4% average yield bogey. However, the rising stock market did not help practitioners of an unmodified “Reverse Dollar Cost Averaging” strategy. The chart below shows that this strategy lost close to 2.5% per year when comparing to a “no-withdrawal” strategy.

From the Pandemic to Today

A practice of maintaining a diversified portfolio, withdrawing from the most stable investments in the portfolio, and rebalancing periodically proved to be adequate during the period of low interest rates from the mid 2010s until 2022. “Income Harvesting” had grown less beneficial as interest rates decreased and the markets increased in value.

High Interest Rates Are Affecting the Economy?

Interest rates rose at a faster pace in 2022 than any time this past century. One-year treasury yields are now close to 10 times what they were at the beginning of 2022, with rates starting under 0.5% and now yielding over 5.0%. This sent bond values plummeting in the short run and caused a strain on the financial system as those who have borrowed to fund business operations, buy cars & homes or other items now find themselves more stretched than they anticipated. The leverage in the system helps to multiply the positive and negative effects of interest rate moves.

What may be harder to see is that the best bond markets of the past followed a similar period of bond decline. This has not transpired yet as we are currently in the midst of the longest yield curve inversion in history. Bond yields typically top either just before or just after a yield curve inversion. The bond market rewards investors handsomely from this topping process to the end of the cycle. It may not be fun to lose 15% to 20% or more investing in bonds during the rate hiking process. However, bonds prove profitable after rates have peaked and protect from these selloffs heading into recessions. In some cases, the differential is over 50%. For more on this, follow the link to, Do You Want Good, Better, or Best?

The rate hikes of the past few years have changed the landscape significantly

Looking back over the past few years, commodities and other Inflation Hedges have outperformed. Focusing a slice of the portfolio on inflation protection has proven to be a profitable strategy since the pandemic and subsequent fiscal stimulus measures. At some point, we feel precious metals and treasury bonds may prove to provide the best protection for investors now that inflation concerns have become less worrisome than the threat of recession and economic instability. In the meantime, looking at repositioning portfolios to an “Income Harvesting” strategy may provide the stability many are looking for.

For those interested in pursuing an “Income Harvesting” strategy, please feel free to email or give our office a call. Laddering a portfolio of CDs and treasury bonds may prove to be more beneficial than many people currently realize, especially if we head into a deep recession as many currently fear.

Franklin Wealth Management

4700 Hixson PikeHixson, Tn 37343423-870-2140