**Since yesterday was a big down day in the market, I’ve got a quick thought at the end of this blog.

Once upon a time in the country there worked a dairy farmer who was having trouble getting his cows to produce milk. They seemed well fed but as the cows grew fatter and fatter, the milk they produced did not ever seem to increase but actually seemed to diminish over time. He grew disheartened by this ever diminishing supply of milk and sought the help of a consultant to help with the milk production. The consultant advised him to sell his current cows at the meat market and he was more than happy to because the dairy farmer received much more from sale than he had originally bought the cows for (they were originally bought by the pound when they were much thinner). The consultant also advised the farmer to buy a different breed of “Yieldstein” cows that did not need consume as much food but provided a higher yield in the form of milk production. Again the dairy farmer was happy because he was able to buy more cows and also generate a greater amount of milk production than ever before.

A few months went by and the cows seemed healthy. The milk production was continuing to increase. But the dairy farmer was starting to grow a little concerned because the cows were not gaining much weight and in fact some seemed to be losing weight, even though milk production for the farm was at an all time high. If one of the cows started to get a little too overweight, the consultant would recommend the farmer sell the cow at the meat market and buy more slimmer cows.

This continued for many months and the dairy farmer’s milk production kept hitting new highs. He kept getting concerned however that his cows were not as fat and seemingly well fed as before. In fact, when he weighed the cows he found that the “Yieldstein” cows weighed less than when he had bought them. He grew nervous and started weighing the cows every day (sometimes even twice a day) whereas before he had never bothered when he had the fat cows. His milk production was at all time highs but he reasoned at this rate of weight loss these cows are going to waste away to nothing in no time.

He called up the consultant and complained that the weight of his cows continued to diminish and he was worried. He did not know what to do. The consultant told him that it was just a seasonal anomaly and that these cows had wider weight fluctuations but would fatten up approaching winter time. A couple more months passed and the cows continued to lose weight but also continued to produce more milk. The farmer started to talk to his other farmer friends who had also bought this alternate breed of cows as well as his friends who had held onto their original cows. He and his friends with the new breed were all generating record milk production from their farms but the cows all kept getting skinnier. Those friends with the original breed of cows were barely surviving because they could not get their cows to produce much milk but the cows all looked fat and healthy.

Some of the farmers friends decided that they had had enough and decided to sell before the cows grew too skinny and died. This continued for a few weeks until the farmer was one of the only ones still owning the skinny cows. He was thinking about calling the consultant and giving him a piece of his mind for talking him into the skinny cow business even though his milk production was still at all time highs. The consultant called and related to him that the price of skinny cows was now at all time lows and that he should look into buying more. Of course the farmer thought he was crazy but decided that the consultant knew what he was talking about and even though he did not buy any more, felt a little better about owning his skinny cow herd.

A few weeks more passed and heading into winter the cows started to get more of an appetite and started to put on weight again until they weighed more than they ever had before. As before when a cow got too fat, the consultant would advise the farmer to sell the fat cow and buy a skinner cow that produced more milk. The farmer did not worry too much about his cows after that, until the next season when they started to get skinny again.

This story is analogous to the past few years as we have seen yields from investment grade bonds continue to shrink as the bonds became more and more pricey, many times trading at steep premiums to par value or the principal amount that will be paid back at maturity. At the same time, currently we see the yield spread between high yield bonds and treasuries at over a 7% differential, which is the highest we have seen since late 2011.

Income oriented stock investments are also giving us higher yields than we have seen in a long time in that they have underperformed the S&P 500 over the last year by a significant margin. The returns for the S&P Global Dividend Aristocrats Index over the past year ended up being negative at -7.43%, although the yield for this index was 4.1%. Does that mean we need to sell all of our income oriented investments? (or skinny cows?) Sectors, Asset Classes and Industries go in and out of favor. Currently income oriented equities do not seem to be overly popular but times change and they will eventually become popular again. Unfortunately, many investors tend to invest in the popular sectors and industries at the top when they may be starting to fade and shun them at the bottom when things are improving. A smart and courageous investor will look to buy “when there is blood in the streets.” For those of us that might not be quite as adventurous, holding onto these unpopular sectors and types of investments tends to work better than selling when prices are down

The Year in Review

2015 gave us some of what we expected as well as some surprises. The economy trudged along, the unemployment rate fell, and the Federal Reserve finally lifted the Fed funds rate at the end of the year.

Taking a closer look, we see what many people are calling “The Tale of Two Economies.” This is because we saw the service industries expand at a modest pace while the stronger U.S. Dollar caused exports to fall, and we also saw huge reductions in the Energy sector which took a toll on manufacturers.

On the equity (stock market) front, the S&P 500 Index ended the year as a loser for the first time since 2008, and the S&P 500 experienced its first 10%+ correction in four years.

China’s economy got blamed for the late summer sell-off but as I look back on the year, the anxiety attached to the overall global economy provided a great excuse for short-term traders to justify hitting the sell button. It will remain unknown if those traders were good (lucky?) enough to then get back in at the bottom, but long-term investors who had no reason to react saw the losses fill back up pretty quickly. Those who decided to abandon their plans, panic and either decided not to get back in or got back in too late felt the most pain this year.

What can we learn here?

You are not able to predict what will happen nor when it will happen…and neither am I.

Probabilities and statistics are on the side of the patient investor who sticks with a plan…but let me get back to my thoughts on 2015 before I get too far off on a tangent.

Even though the S&P 500 was slightly negative for the calendar year (-0.7%), growth stocks significantly outperformed value and large companies did better than smaller companies. If we compare the S&P 1000 Value to the S&P 1000 Growth Index, growth outdid value by a staggering 9.27% with the S&P 1000 Value Index losing 8.32% for the year. Many of you may already be aware that the FANG stocks (Facebook, Amazon, Netflix and Google) accounted for most of the gains in the S&P 500 and without these stocks would have been much more negative. With the FANG Stocks returning over 80% in 2015 it was a very profitable year to be somewhat irrational. Considering the average price earnings ratio for these four is over 60 with a price to sales ratio over 9, investors are definitely paying a high price for a cheery consensus (see Warren Buffett article circa 1979 here).

The smaller companies did not fare as well as a whole but there was less dispersion between the growth companies and the value companies with the Russell 2000 averaging -5.71% for the year and the growth vs. value disparity at 7.22% in favor of growth.

Over time it is hard to say whether growth performs better than value or vice versa. Some studies will show that value outperforms growth over time whereas others show that growth outperforms.

The results are most influenced by the time periods used for the studies. However in weak market periods most studies show that value outperforms whereas growth tends to outperform in stronger market periods.

For this reason we recommend that investors have a mix of growth and value holdings in their portfolio although we have a bent toward value companies for more conservative investors because they tend to sport higher dividend yields and tend to carry a wider “margin of safety” (see Benjamin Graham’s central concept here)

Overseas, the strength of the dollar hurt returns for U.S. (dollar denominated) investors, with developed markets up marginally because of respectable returns out of Japan. Emerging markets and commodities both labored as the increase in the U.S. dollar and the specter of a global growth slowdown (thanks China) acted as a big drag on returns.

With the exception of U.S. high yield, which was crushed due to the weak Energy sector, fixed income markets were essentially flat.

Despite the overwhelming beliefs that we would see a hike in the fed funds rate and the actual trigger pulled by the Fed in December, 10-Year Treasury yields remain at historically low levels. I think this has a lot more to do with the fact that inflation and growth expectations in the U.S. remain low, but it’s also probable that the very low government bond yields in Europe may be playing a role in this as well. In a digital world where cash can rapidly move from country to country, European capital seeking a relatively higher yield in the U.S. will go into U.S. Treasury bonds. This has the effect of driving prices higher, which then drives the yield (the interest paid on the bond) lower…so the U.S. Treasury yields stay lower. (Remember, when dealing with bonds, yields go down when prices go up and vice-versa.)

Looking Out to 2016

Gazing into the upcoming year is always fraught with peril. I don’t have a crystal ball…all I have are statistics, probabilities, information and my brain to make sure ideas are grounded in reasonableness. We are now entering the eighth year of this bull market and while that seems to make a lot of people nervous, the length of a bull market does not forecast a demise.

As of now, we do not see many signs pointing to a recession right around the corner.

How the market does in 2016 will depend on both the economy and corporate profits. The start of a new calendar year does not mean that the issues from 2015 (poor corporate earnings, the flat global economy, the strong U.S. Dollar, and low commodity prices/oil) are “last year’s issues.”

Earnings in 2015 and 2016 (estimates)

Earnings are a huge deal because there is an almost one-for-one correlation between them and the equity markets. This means the two essentially move in lockstep. Thanks in large part to the steep drop in oil prices, profits at energy-related firms took a huge dive last year (reference the sector return I mentioned above). This created a big headwind for overall corporate profits last year. An interesting aside as far as this is concerned is that many refiners actually saw higher profits last year and energy transport company earnings were pretty stable with moderate gains in profitability for most.

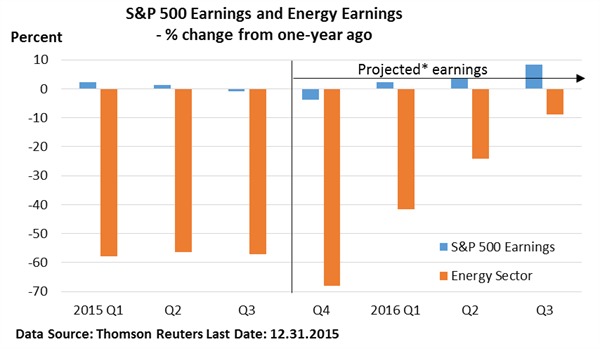

Third quarter (Q3) 2015 earnings, which were down -0.8% from the year prior, would have been about seven percentage points higher if Energy had been excluded (according to FactSet Research). Just look at this chart from Charles Sherry which uses Thomson Reuters. Orange shows the Energy sector earnings and blue represents the earnings of the entire S&P 500 index.

Throw in the stronger U.S. Dollar along with the fact that multinational companies earning money overseas must convert it back into U.S. Dollars and they lose money just because…

The blue bars also show that analysts are expecting earnings to turn positive in Q1 2016 and accelerate as the year progresses. We will see, but even low growth in profits would probably be helpful for stocks in 2016. Also, I think a lot of analysts are expecting earnings to be better based on a continuation of the U.S. economic expansion, a bottom in oil prices, and greater stability in the dollar. Like me, most analysts don’t think a recession is in the cards but the direction of the dollar and oil is a bit harder to predict.

The forecast for rising profits is cautiously encouraging. Just look at what all the analysts are predicting across all the great research shops and average them together since everyone is making educated guesses based on what companies feel like guiding them on anyway.

Will Oil and Commodities ever recover? What about the dollar?

These low commodity prices have benefitted nearly everyone outside of the energy industry, emerging market economies and companies in the mining industry.

Blame the drop in commodity prices on China, which seems to be converting from an industrial economy to a balance between a consumer/services and goods producers economy, slowing their appetite for raw materials. When demand slows and supply increases, prices go down…and in this case to the lowest level in over a decade.

Commodities are also massively impacted by the U.S. Dollar because most are priced in dollars. So, our rising U.S. currency puts downward pressure on prices. This is great for consumers but bad for producers. Simple, I know, but worth pointing out.

Falling prices then negatively impact global sentiment, which then makes its way into the broader stock market. From there, you get the Energy sector experiencing sizable layoffs among oil producers and big cutbacks in capital spending. That brings you back full circle to earnings (above).

However, it’s not just the strong U.S. Dollar, it’s also soaring production of shale oil in the U.S., which has helped create a global oversupply of crude and a drop in U.S. imports.

Looking ahead, what happens to China and the dollar will likely have an influence on the Commodity sector this year. But what occurs in the U.S. oil fields will also play a role. Greater stability would lessen the uncertainty for investors. However, trends in commodities, including oil, tend to move in long-term cycles.

Finally, without getting too much into junk bonds, there is a fear that the current commodity market issues will cause energy companies to default on their debt. If the Commodity sector remains stable at current levels, this issue is not likely create the amount of defaults that people fear. Those with long-term debt exposure in this sector should maintain patience.

Wrapping Up

I still stick to the fact that the consumer is responsible for 70% of GDP, and that housing and cars drive second and third (and more) order effects in our domestic economy, and both are strong.

The most likely path in 2016 is probably just an extension of 2015 although one can expect many undervalued areas to catch up with overvalued areas like we typically see over time. 2016 will probably see a modest, continued and unimpressive economic expansion that adds a little tailwind to corporate profits.

Again, I don’t have any idea what the future holds. Ultimately, the U.S. economy has the biggest effect on markets. A lot of fear I hear these days comes from investors who worry about a terrorist attack. One thing worth remembering is that following the 9/11 attacks on our country, the S&P 500 fell around 12% in the first five trading days, but had completely erased losses by October 11, 2001.

I May Be Repeating Myself

My recommendations for investors in 2016 are:

- Have a long-term financial plan and an appropriate investment strategy that supports that plan.

- You should have access to cash to meet your liquidity needs for12-18 months so you are not forced to panic or make emotional reactions to market pull backs like we saw last summer, or in 2012…or 2011…or 2008/9.

- Stay invested in sectors of the market which, during the expansion phase of the economic cycle, have a higher probability of outperforming others.

I catch a fair amount of good natured ribbing for espousing the same advice over and over. I get it, a lot of people expect folks in my business to always be “doing something.”

I like defending myself when I’m right…or at least, not wrong…but the reality is that “doing something” seems stupid to me when for the last eight years we have not seen a whole lot of change. We continue to see low interest rates, low inflation, modest GDP growth, and no over-spending, over-confidence or over-borrowing. Not much has changed, except oil prices are putting a lot of money back into consumers’ pockets.

We make tweaks to the underlying sectors and individual stocks in our portfolios but for the most part, staying allocated to small and mid-cap growth, cyclical sectors of the S&P 500 and maintain some global holdings, although we hold very little China exposure currently.

Historically, the long-term investor that adheres to a professionally crafted investment plan is more likely to achieve his or her financial objectives. If your personal situation has changed, let’s talk.

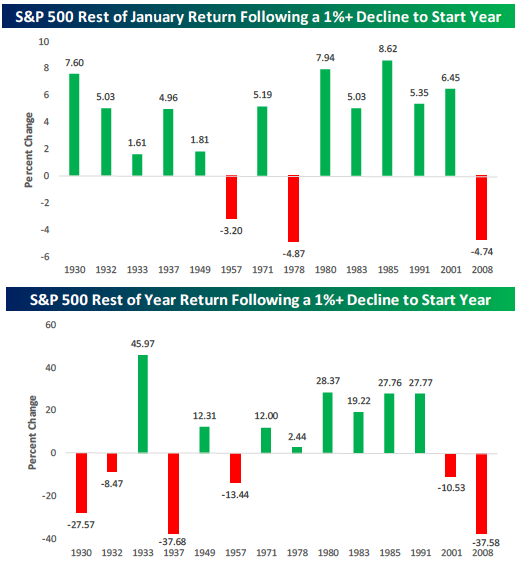

Finally, About Yesterday: January 4, 2016

This chart below is from Bespoke.

Data as of 12/31/2015

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, a registered investment advisory firm in Hixson, Tennessee. A 20-year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be investedinto directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.