You’ve likely noticed all the ads for brokerage custodian firms rapidly slashing the cost of trades to zero on some of their most popular items, notably stocks and exchange-traded funds (ETFs).

At Franklin Wealth Management, we had already negotiated with our two custodian firms, TD Ameritrade and LPL Financial to reduce costs for our clients. Franklin Wealth has been paying the trading costs and passing the savings on to clients. Many costs have been reduced over the years, especially when we were able to eliminate most 12B-1 fees a couple of years ago within mutual fund models. With TD Ameritrade dropping trading costs on Stocks and ETFs to zero, we are going to be able to reduce our fees by 5 Basis Points on all Stock and ETF models held at TD Ameritrade starting in November.

Why long-term investors stand to benefit the most

While investors should be cheering the news, not all of them stand to benefit, depending on how the industry shapes up. But investors do have several moves they can make to ensure that the industry’s price-slashing does indeed benefit them.

First, it’s great that clients can avoid commissions on stocks and ETFs. That’s money that can go right back into their pocket.

But, will the lure of zero commissions actually cause investors to trade more often? If so, that could be quite dangerous for their wealth, since study after study shows that “time in the market” is one of the best predictors of an investor’s return and that day-traders typically lose money. While the savings may initially benefit short-term investors, it’s money that may ultimately be lost in the market as they continue to ring up losses. Below is a 20 year Dalbar study that notes the difference between a “buy and hold” strategy and average investor performance caused by trading too often. Unfortunately, zero costs may exacerbate this trend.

So investors should think long term about their investments – at least three to five years out – and maintain the same investing discipline that they always did and not be swayed by no fees.

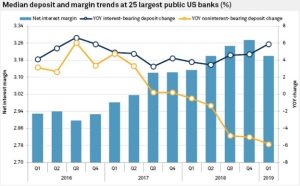

Second, brokers might make up the shortfall by paying you even less on cash balances in your account.

Schwab generates 57 percent of its revenue from interest, and that’s the difference between what it earns on that money and what it pays clients. So, the broker may seek to expand that margin by lowering what it pays out.

That, of course, is unfavorable to clients holding cash in their accounts.

If as a response to this price cut, brokers move to pay even less on your cash balances, it could be wise for you to take matters into your own hands to ensure you’re maximizing your money.

For example, through your brokerage you can usually buy insured bank products such as CDs or municipal bonds (which look particularly attractive currently). Or you can otherwise easily move that money out of the brokerage account and into a bank’s CD or savings account until it’s needed at the broker.

Alternatively, you can make investments in other very low-risk products that earn a bank-like yield. Please feel free to contact us about these other alternatives.

Third, investors can benefit by using free trades to practice dollar cost averaging more effectively – even with ETFs.

Dollar cost averaging means buying fixed dollar amounts of stock over periods of time. The practice averages out your buy price and may help you profit more.

Before, dollar-cost averaging into investments other than mutual funds could get expensive and cut into returns even if you were investing a few hundred dollars regularly. Now, thanks to free trades, even investors with small amounts of money can add to their positions and take advantage of dollar-cost averaging.

As you can see from the chart above. One investor is able to invest everything at once and as the market fluctuates, ends up with a 0% return after a few months, while another investor who is dollar cost averaging makes 4% over the same time period. This is great for those investors who are saving into a volatile market, stock, ETF or fund. However, the opposite happens when investors are withdrawing funds. In one of our next articles we plan on detailing some of the strategies and tactics we use to mitigate this volatility risk.

Finally, if free trades cause investors to trade more often, then it becomes even more important for investors to stick to their long-term mentality.

Not only will they avoid the increased likelihood of losing money on short-term trades, but they’ll also minimize the effect of high-frequency traders on their portfolio. Volatility is likely to increase as more people grow more active because of free trades. If you buy and hold long-term, the few pennies on a trade that these traders scalp on each share will make no real difference to your long-term return.

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, and CEO of Innovative Advisory Partners, a registered investment advisory firm in Hixson, Tennessee. A 20+year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are un-managed and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.