“History shows that lending and spending on items that produce broad-based productivity gains and return on investment that exceed the borrowing costs result in living standards rising with debts being paid off, so these are good policies.” – Ray Dalio

There are a lot of things to be optimistic about in the most recent infrastructure bill that was passed by both houses today. Both parties agreed on the bill and most Americans can agree that smart spending on these needed items have potential.

The proposed spending looks to be productivity enhancing in the long run and may provide additional stimulus in the short run. How this is put in place will show us the extent this spending may benefit the country and our economy. In addition, almost all of the funds for this infrastructure bill are already paid for. Any upcoming impasse over debt ceilings is less likely to derail this spending. With the recent gains in state and local elections, will Republicans still want to threaten a government shutdown? We feel this is less likely but still probable.

What to Expect and Prepare for During the Holidays.

The period heading into the Holidays is typically the strongest period of the year for the markets as investors feel the urge to spend for others and invest for themselves. We anticipate this will be the case again in 2021 but see that the road is full of more speed bumps than usual for this time of year. With significant gains in the market since the lows of 2020, we are already starting to see adjustments being made as investors are offsetting these gains by selling whatever they can in their portfolios at a loss. In our model portfolios it has been hard to find much to sell to offset these realized gains in taxable accounts, however. Because of this we have started to invest in Opportunity Zone Reits to defer some of these gains. If the market continues to rally, this may allow us to free up additional unrealized losses to offset these gains. When the market dips or crashes, any potential losses can be offset and equalize against the deferred gains.

The Build Back Better Bill contains many potential tax increases, many of which are proposed to be retroactive. It will likely only be passed via reconciliation if they can find the support of the Moderate Democrats. The final form is likely to contain some but not all of these tax increases. We feel it is best to be prepared for these tax increases and will be hosting another webinar class on these in the near future.

Many Feel the Bond Market Is Predicting a Federal Reserve Policy Mistake.

Chairman Jerome Powell announced earlier this week that they would start tapering their asset purchases later this month. This means that they will still be stimulating but trying to reduce the level of stimulation as they work to take the U.S. economy off economic life support. Some feel this tapering will lead to tightening which may eventually kill the economy. Others feel that tapering and tightening may be necessary sooner than most expect to fight off inflation.

Yield curves are flatter than many might expect at this point with the 30-year yield dipping lower than the 20 year yield. A flat yield curve becoming an inverted yield curve is typically a precursor to recession in the coming months. We usually see the inversion show up where the 10-year yield is less than the 2 year yield. Much like negative energy prices in the midst of the 2020 pandemic, we are seeing something extremely novel. The one thing we can say about this is that it seems the Federal Reserve fears that the worst will happen if it were to take its hands off the wheel.

What about Inflation?

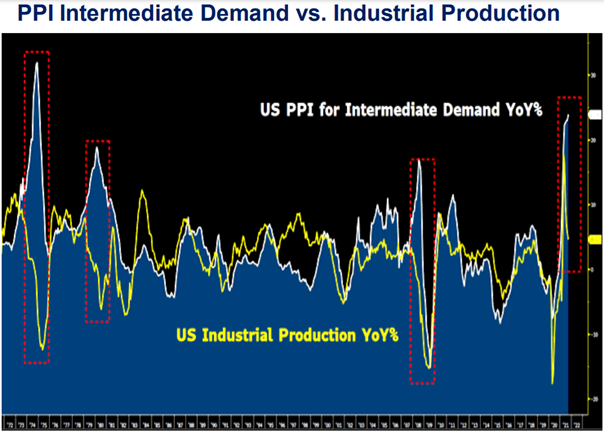

Its hard to find someone who has not felt the impact of the gasoline tax or the grocery tax on their pocketbooks. Many feel these high prices in commodities, cars and lodging are anything but transitory. What is even more troubling than the consumer inflation we have been experiencing is the amount of inflation experienced by companies as prices they are paying has increased even more than the prices they may be passing on to their customers. This Producer Price Inflation has ramped up over 20% since last year and sits at levels we have not seen since the early 1970s. Those companies that can in turn raise prices to customers will be in much better shape going forward than those without this pricing power. Unfortunately, we are already starting to see profit margins deteriorate. The markets have not factored this in yet but may in the near future.

To quote Larry McDonald from the Bear Traps Report: “What we have here, ladies and gentlemen, is a consumer buying panic. We lived through this movie before in the 1970’s and early 1980’s. It isn’t pretty but it also creates great short-term earnings. So short term rates spike and companies with positive guidance rally. But eventually the economy collapses, and stocks get crushed. That huge wad of cash being spent so frenetically is both raising inflation, the cost of debt and now, as latest GDP data confirm, slowing the economy down. This stagflation will show up in earnings going forward, and in a bad way. We want to look closely at the Producers Price Index, which is well over 20% higher than a year ago. Not all this increase in the cost of production will be passed on to the consumer. That means profits will shrink and forward guidance will come down causing stocks to sell off eventually.”

“Inflation could be “much worse” than feared… It’s probably the single biggest threat to certainly financial markets and probably I think to society just in general.” “I’m just worried about the future of this country… the most inappropriate monetary policy that I’ve seen [pauses] maybe in my lifetime.” – Paul Tudor Jones

Do Valuation Metrics Still Matter?

Recently a team member made a statement that he felt many valuation metrics used over the last century may no longer be as viable. Using relative valuation metrics and measurements based upon assumed correlations have become more commonplace. We have found through internal and external studies that some of the best metrics to measure against are those that are the hardest to fake. Dividend yields have proven extremely difficult to fake in that we know immediately if the company is paying us regularly or not. Revenues also tend to be harder to fake than profits, although some companies have developed ways to inflate these numbers as well. Fraudulent accounting becomes more and more commonplace as we march toward manic periods where investors are experiencing a fear of missing out.

We have produced charts of the “Buffett Indicator” many times over the last couple of years. Warren Buffett is known to promote this indicator as one of the best to determine how under or over-valued the markets may be. This indicator, as shown below compares the total market cap of all companies traded within the U.S. to the U.S. GDP. The chart below clearly shows that we are currently in all time high territory and every time we have reached these levels in the past, the returns over the next ten years were negative. But, as we have noted before, markets can and do continue to move higher, even when we may think they have no more room to run.

Where do we see Opportunities?

In almost all time periods, there are places to invest where we can find attractive values. Currently the most attractive values can be found in emerging markets. These markets may continue to get cheaper, but when they start to turn around, we see more upside over the long term. We have noted that many professional investment managers we admire are actively buying Chinese technology companies currently.

Last year, commodities and energy in particular looked extremely cheap as investors were paying others so that they would not have to take delivery. Negative prices are exceedingly rare, but this is what we saw when all storage facilities were filled to the brim. Of course, we are now concerned about inflation and prices are continuing to march higher. We want to do what we can to protect from this inflation by owning energy companies, REITs, mining companies, and other investments that can benefit from higher prices in the future. Blockchain investments also fit this mold as many consider NFTs and cryptocurrencies to be commodity-like. Scarcity rules in today’s markets. We want to own scarce assets as there is more currency chasing fewer and fewer goods.

Diversification is almost always a good idea. Diversifying into multiple investments that you understand well, is an even better idea. Diversification into a few temporarily undervalued investments with significant upside that you understand well tends to provide the best results over time.

Joe D. Franklin, CFP is Founder and President of Franklin Wealth Management, a registered investment advisory firm in Hixson, Tennessee. A 20+year industry veteran, he contributes guest articles for Money Magazine and authors the Franklin Backstage Pass blog. Joe has also been featured in the Wall Street Journal, Kiplinger’s Magazine, USA Today and other publications.

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.