The “Backdoor” Roth IRA Is Currently in the IRS Crosshairs?

For the time being, the Backdoor Roth IRA is a legitimate strategy for many high earners to get money into after-tax accounts. One of the provisions of the “Build Back Better Bill” is to disallow the conversion of all after tax amounts. This would eliminate a strategy that in one case, allowed us to save a client over $60,000 in taxes on a botched conversion For more on this please refer to this Wall Street Journal Article link.

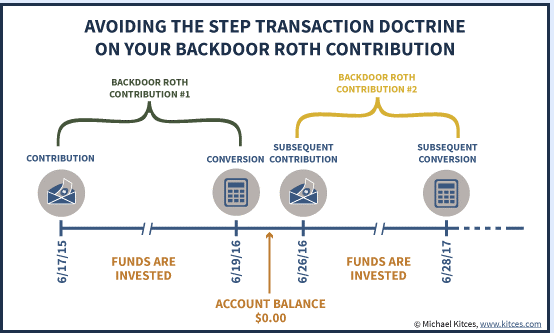

Under what is referred to as “Step Transaction Doctrine”, the Tax courts have ruled previously that transactions performed in rapid succession with no business purpose could incur further scrutiny and be deemed impermissible. In order to protect against such a transactions being disallowed due to potential scrutiny in the future it is advisable to allow any non-deductible contributions an incubation period of at least one month prior to performing the Roth Conversion.

Using non-deductible IRA contributions and later converting into Roth IRA’s while paying little to no taxes can be a worthwhile strategy for those that would like to access Roth IRA’s but are currently restricted from making direct contributions due to their earnings. Unfortunately, this may be the last year to do so.

Paying Attention to the Details

We had been making these non-deductible IRA contributions for both the husband and the wife for several years to save additional funds on a tax-deferred basis as they were already maximizing 401(k) contributions. Once the income limitations were abolished on Roth Conversions in 2010, we began converting these non-deductible IRA contributions to Roth IRA’s with little taxes due on the conversion. Neither the client nor his wife had any IRA’s outside of the non-deductible IRA’s, so this wasn’t complicated by what is known of as the IRA Aggregation Rule which will be explained later. Upon contacting their tax preparer about the Roth conversion in question, we learned they had not included the Form 8606 for non-deductible IRA contributions on the current return.

While many high income earners are excluded from making direct Roth IRA contributions they are often able to make non-deductible IRA contributions and later convert these accounts to Roth IRA’s without any taxes due on their non-deductible contributions. Any growth in value will be taxed as ordinary income at the time of the conversion. It is important to note that you must keep track of these non-deductible IRA contributions via timely filing of the Form 8606 with the IRS in the year of the contribution.

The “Build Back Better Bill” is looking to eliminate not only these “Back Door” Roth contributions but also the conversion of after tax amounts in 401ks and IRAs from years gone by. Some have been able to contribute additional lumps into 401ks as after tax contributions in recent years and convert much more than the IRA limit of $7000 per year per person by using these “Mega Back Door Roth’s” in 401ks in recent years. Considering this may be the last year to take advantage of the conversion of these after tax contributions, we want to make sure that everyone is aware, reviews these 8606 forms to make sure they convert everything possible, and do this in the most efficient way, before it is too late.

Watch out for the IRA Aggregation Rule and Pro-Rata Taxation

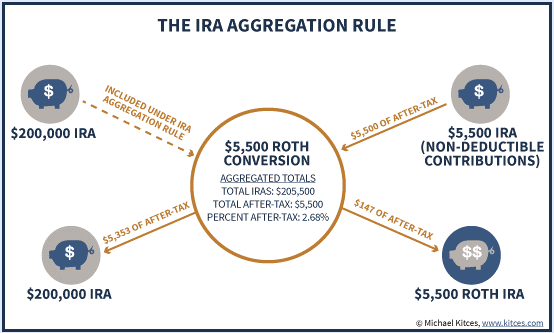

There is one other caveat to ensure the conversion is tax-free, the owner should not have any other IRA’s at the time of the conversion. If other IRA accounts exist (includes SEP IRA’s and Simple IRA’s but does not include any IRA’s owned by the spouse) then the conversion will be subject to IRA Aggregation and pro-rata taxation of the conversion. To illustrate this, let’s suppose someone has pre-tax IRAs worth $200,000 along with $5,500 in non-deductible IRA contributions prior to making a conversion. Of the $205,500 in total IRA balance 97.3% is pre-tax and 2.7% is after-tax. Even if they convert only $5,500, the conversion will be 97.3% taxable and 2.7% tax-free. So in essence, they will pay ordinary income tax on $5351.50 and only $148.50 will be tax-free at the time of the conversion.

Using Your 401(k) or Employer-Sponsored Plan to Avoid the IRA Aggregation Rule

Those that have IRA’s already may still be able to take advantage of this through proper planning. Since only IRA’s (Traditional, SEP & Simple) are subject to IRA Aggregation, 401(k)’s, 403(b)’s, Profit Sharing Plans, etc. are not included in the calculation. If your employer allows rollovers into their plan, you can roll over any other IRA’s into your plan at work. 401(k)’s and other like plans will only allow pre-tax contributions to be rolled in. This would allow you to convert only the nondeductible IRA to a Roth IRA allows for a potentially tax-free conversion.

But, it is important to be aware that this year may be the last year to do so.

Backdoor Roth IRA Checklist

- Verify there are no other pre-tax IRAs.

- If there are, rollover existing pre-tax IRAs to a 401(k) (if available) to avoid the IRA aggregation rule

- Contribute to non-deductible IRA.

- Invest funds in the non-deductible IRA

- Keep invested for up to 1 year.

- Convert to Roth IRA

- File IRS Form 8606 in the year any non-deductible contributions are made.

- Repeat steps annually as desired

Important Disclosure Information for the “Backstage Pass” Blog

Please remember that past performance may not be indicative of future results. Indexes are unmanaged and cannot be invested into directly. Index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investments. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Franklin Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Franklin Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Franklin Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Franklin Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.